Temporal Disaggregation and Interpolation of a Time Series using the Model-Based Denton Proportional Method

Source:R/mbdenton.R

denton_modelbased.RdThe Denton proportional first difference (PFD) method can be expressed as a statistical model in a state-space representation. This formulation provides increased flexibility, including the ability to incorporate outliers, which correspond to level shifts in the Benchmark‑to‑Indicator (BI) ratio, that would otherwise induce unintended wave effects under the standard Denton PFD method. In addition, the approach allows the disaggregated series to be constrained (or 'frozen') at specific periods or prior to a given date by fixing the corresponding high‑frequency BI ratios.

Usage

denton_modelbased(

series,

indicator,

differencing = 1L,

conversion = c("Sum", "Average", "Last", "First", "UserDefined"),

conversion.obsposition = 1L,

outliers = NULL,

fixedBIratios = NULL

)Arguments

- series

A low-frequency time series to be disaggregated or interpolated. It must be either a

"ts"object or a numeric vector.- indicator

A high-frequency indicator series. It must be of the same class as

series.- differencing

Not yet implemented. This should be left equal to

1(corresponding to the Denton PFD method).- conversion

A character string specifying the conversion mode, typically

"Sum"(the default) or"Average". Other options are:"Last","First"and"UserDefined".- conversion.obsposition

An integer specifying the position of the low-frequency observations within the interpolated series (e.g. the 7th month of the year). This argument is used only for interpolation when

conversion = "UserDefined".- outliers

A list specifying the outlier periods and their magnitude. Each element must be provided as

"YYYY-MM-DD" = value, where the date identifies the period. The numeric value specifies the intensity of the outlier and corresponds to the relative value of the innovation variance (with1indicating the normal situation).- fixedBIratios

A list specifying the periods for which the Benchmark‑to‑Indicator (BI) ratios should be fixed. Each element must be provided as

"YYYY-MM-DD" = value, where the date identifies the period and the numeric value specifies the fixed BI ratio.

Value

An object of class "JD3_MBDENTON_RSLTS" is returned. The following are returned invisibly as a list:

estimation[[1]]disaggregated Time-Series, BI ratios and standard deviations;likelihood[[2]]likelihood statistics.

See also

For more information, see the vignette:

utils::browseVignettes(), e.g. browseVignettes(package = "rjd3bench")

Examples

# Retail data, monthly indicator

Y <- rjd3toolkit::aggregate(rjd3toolkit::Retail$RetailSalesTotal, 1)

x <- rjd3toolkit::aggregate(rjd3toolkit::Retail$FoodAndBeverageStores, 4)

td <- denton_modelbased(Y, x, outliers = list("2000-01-01" = 100, "2005-07-01" = 100))

y <- td$estimation$edisagg

# qna data, quarterly indicator

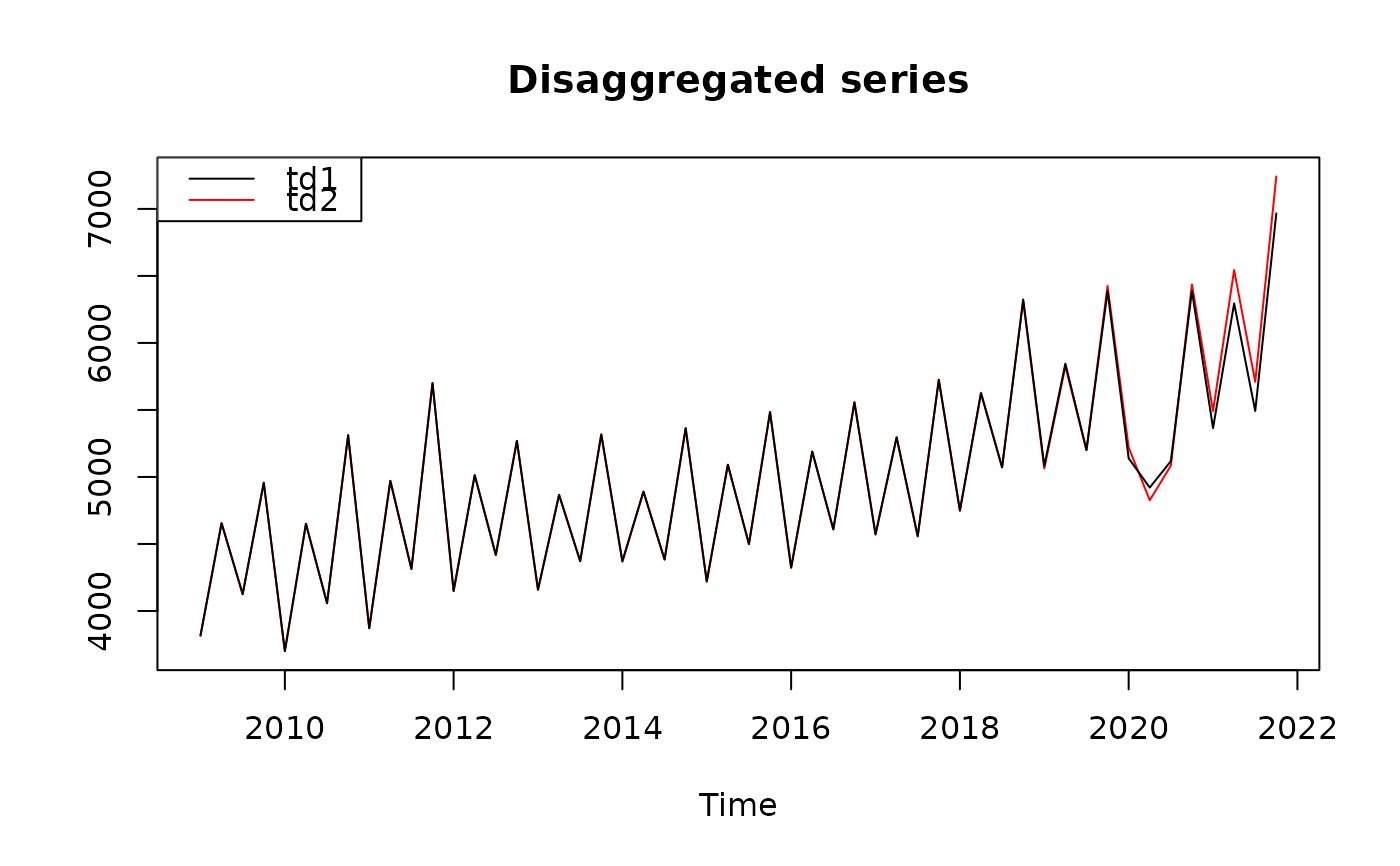

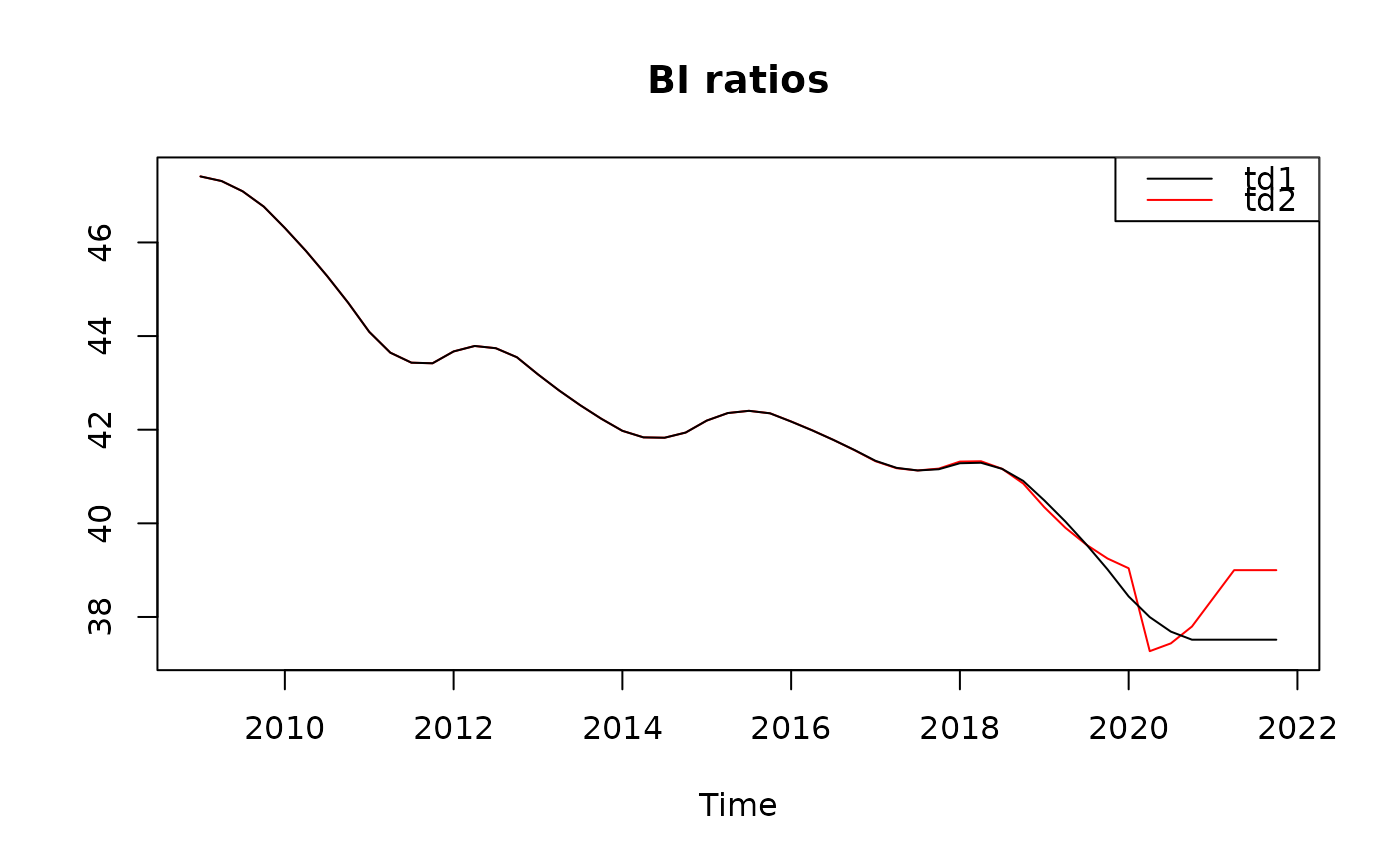

data("qna_data")

Y <- ts(qna_data$B1G_Y_data[,"B1G_FF"], frequency = 1, start = c(2009,1))

x <- ts(qna_data$TURN_Q_data[,"TURN_INDEX_FF"], frequency = 4, start = c(2009,1))

td1 <- denton_modelbased(Y, x)

td2 <- denton_modelbased(Y, x, outliers = list("2020-04-01" = 100),

fixedBIratios = list("2021-04-01" = 39.0))

bi1 <- td1$estimation$biratio

bi2 <- td2$estimation$biratio

y1 <- td1$estimation$disagg

y2 <- td2$estimation$disagg

stats::ts.plot(bi2, bi1, main = "BI ratios",

gpars = list(col = c("red", "black")))

graphics::legend("topright", lty = 1, col = c("black", "red"),

legend = c("td1", "td2"))

stats::ts.plot(y2, y1, main = "Disaggregated series",

gpars = list(col = c("red", "black")))

graphics::legend("topleft", lty = 1, col = c("black", "red"),

legend = c("td1", "td2"))

stats::ts.plot(y2, y1, main = "Disaggregated series",

gpars = list(col = c("red", "black")))

graphics::legend("topleft", lty = 1, col = c("black", "red"),

legend = c("td1", "td2"))