RegARIMA model, pre-adjustment in X13 and TRAMO-SEATS

Source:R/jregarima.R, R/regarima.R

regarima.RdThe regarima/regarima_x13/regarima_tramoseats functions remove deterministic effects from the input series (e.g.calendar effects, outliers)

using a multivariate regression model with arima errors.

The jregarima/jregarima_x13/jregarima_tramoseats functions do the same computation but return the Java objects instead of

a formatted output.

Usage

jregarima(series, spec = NA)

jregarima_tramoseats(

series,

spec = c("TRfull", "TR0", "TR1", "TR2", "TR3", "TR4", "TR5")

)

jregarima_x13(series, spec = c("RG5c", "RG0", "RG1", "RG2c", "RG3", "RG4c"))

regarima(series, spec = NA)

regarima_tramoseats(

series,

spec = c("TRfull", "TR0", "TR1", "TR2", "TR3", "TR4", "TR5")

)

regarima_x13(series, spec = c("RG5c", "RG0", "RG1", "RG2c", "RG3", "RG4c"))Arguments

- series

an univariate time series

- spec

the model specification. For the function:

regarima: an object of classc("regarima_spec","X13") or c("regarima_spec","TRAMO_SEATS"). See the functionsregarima_spec_x13 and regarima_spec_tramoseats.regarima_x13: the name of a predefined X13 'JDemetra+' model specification (see Details). The default value is "RG5c".regarima_tramoseats:the name of a predefined TRAMO-SEATS 'JDemetra+' model specification (see Details). The default value is "TRfull".

Value

The jregarima/jregarima_x13/jregarima_tramoseats functions return a jSA object

that contains the result of the pre-adjustment method without any formatting. Therefore, the computation

is faster than with the regarima/regarima_x13/regarima_tramoseats functions.

The results of the seasonal adjustment can be extracted with the function get_indicators.

The regarima/regarima_x13/regarima_tramoseats functions return an object of class "regarima"

and sub-class "X13" or "TRAMO_SEATS".

regarima_x13 returns an object of class c("regarima","X13") and regarima_tramoseats,

an object of class c("regarima","TRAMO_SEATS").

For the function regarima, the sub-class of the object depends on the used method that is defined by

the spec object class.

An object of class "regarima" is a list containing the following components:

- specification

a list with the model specification as defined by the

specargument. See also the Value of theregarima_spec_x13andregarima_spec_tramoseatsfunctions.- arma

a vector containing the orders of the autoregressive (AR), moving average (MA), seasonal AR and seasonal MA processes, as well as the regular and seasonal differencing orders (P,D,Q) (BP,BD,BQ).

- arima.coefficients

a matrix containing the estimated regular and seasonal AR and MA coefficients, as well as the associated standard errors and t-statistics values. The estimated coefficients can be also extracted with the function

coef(whose output also includes the regression coefficients).- regression.coefficients

a matrix containing the estimated regression variables (i.e.: mean, calendar effect, outliers and user-defined regressors) coefficients, as well as the associated standard errors and t-statistics values. The estimated coefficients can be also extracted with the function

coef(whose output also includes the arima coefficients).- loglik

a matrix containing the log-likelihood of the RegARIMA model as well as the associated model selection criteria statistics (AIC, AICC, BIC and BICC) and parameters (

np= number of parameters in the likelihood,neffectiveobs= number of effective observations in the likelihood). These statistics can also be extracted with the functionlogLik.- model

a list containing information on the model specification after its estimation (

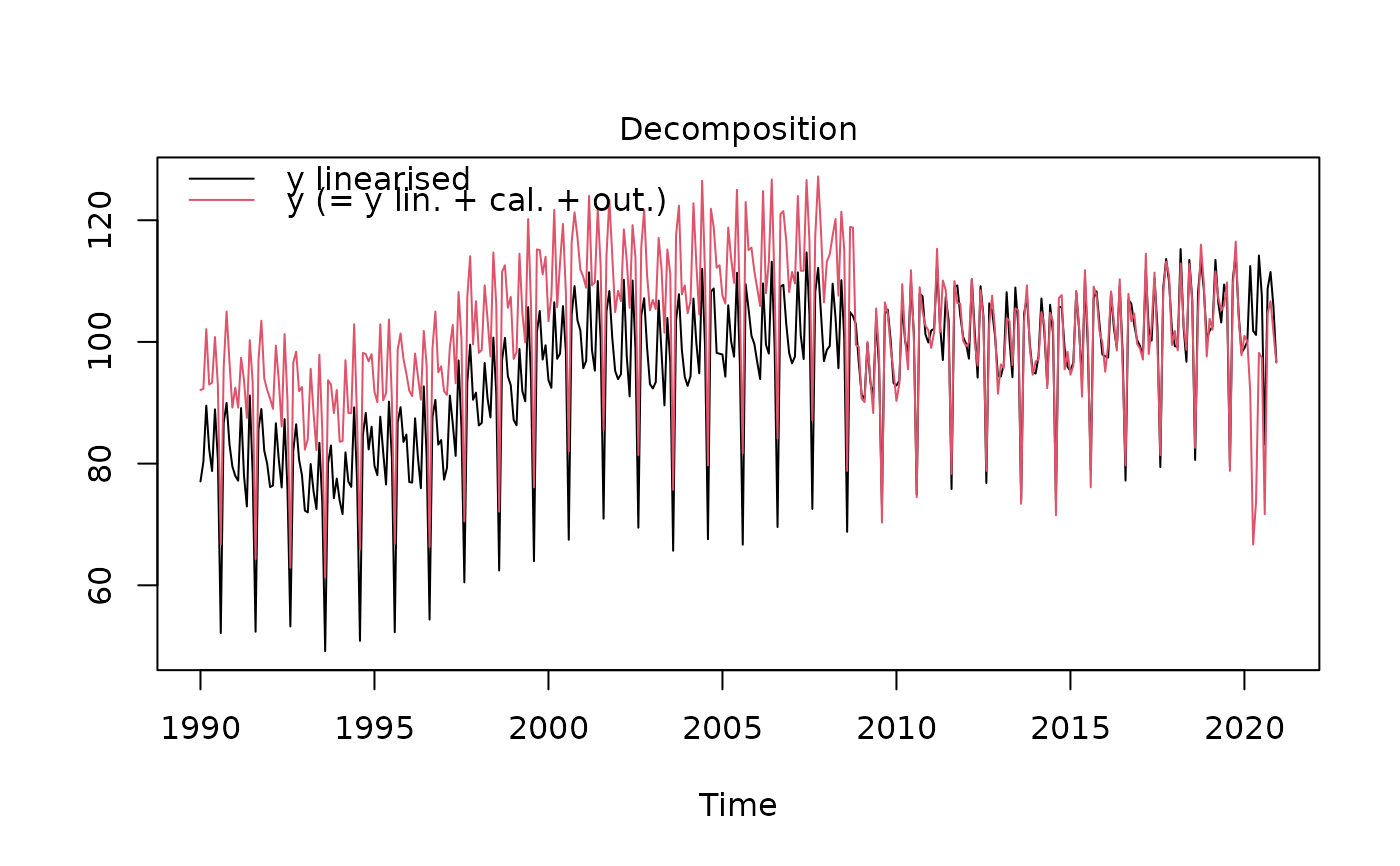

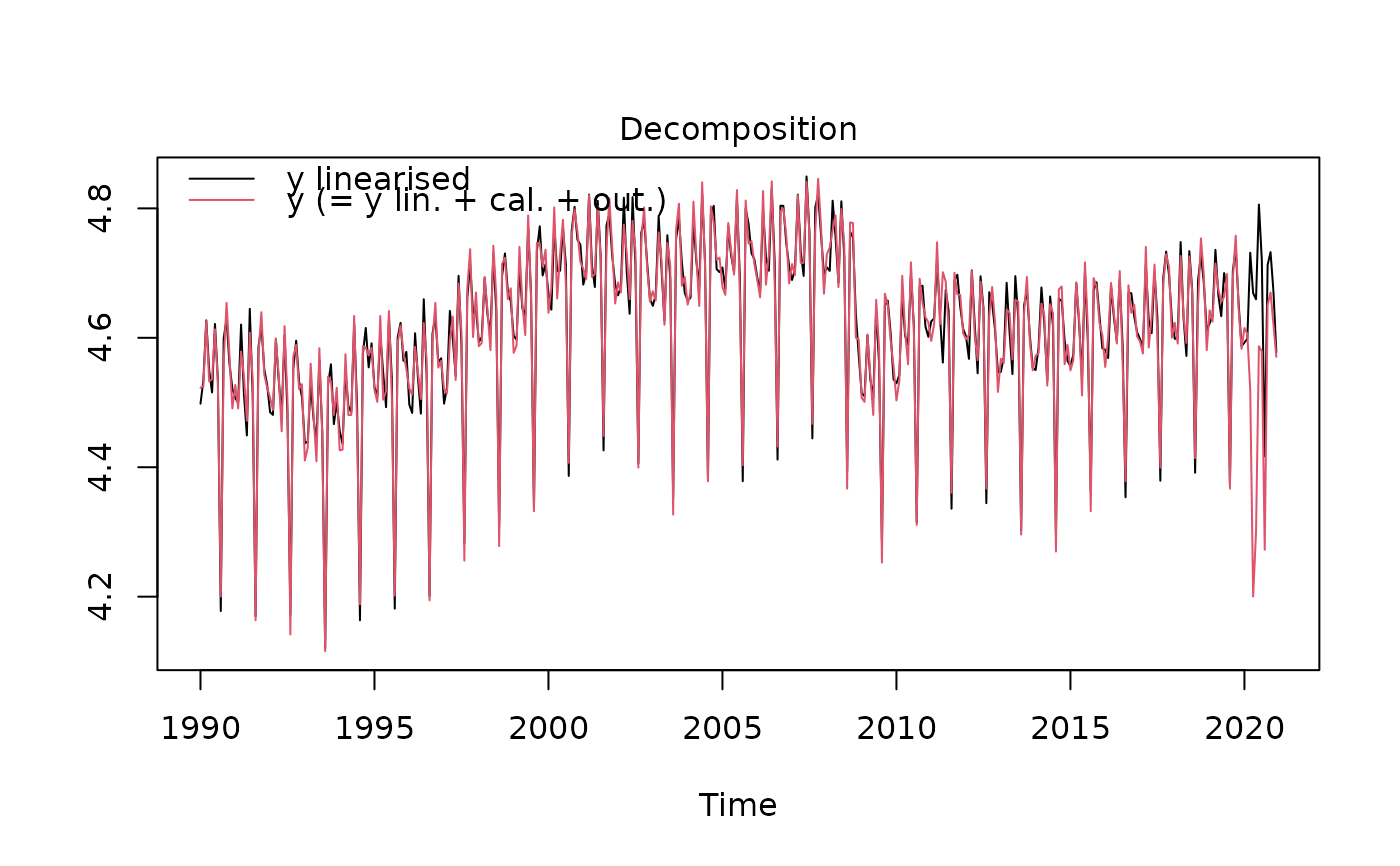

spec_rslt), as well as the decomposed elements of the input series (ts matrix,effects). The model specification includes information on the estimation method (Model) and time span (T.span), whether the original series was log transformed (Log transformation) and details on the regression part of the RegARIMA model i.e. if it includes aMean,Trading dayseffects (if so, it provides the number of regressors),Leap yeareffect,Eastereffect and whether outliers were detected (Outliers(if so, it provides the number of outliers). The decomposed elements of the input series contain the linearised series (y_lin) and the deterministic components i.e.: trading days effect (tde), Easter effect (ee), other moving holidays effect (omhe) and outliers effect (total -out, related to irregular -out_i, related to trend -out_t, related to seasonal -out_s).- residuals

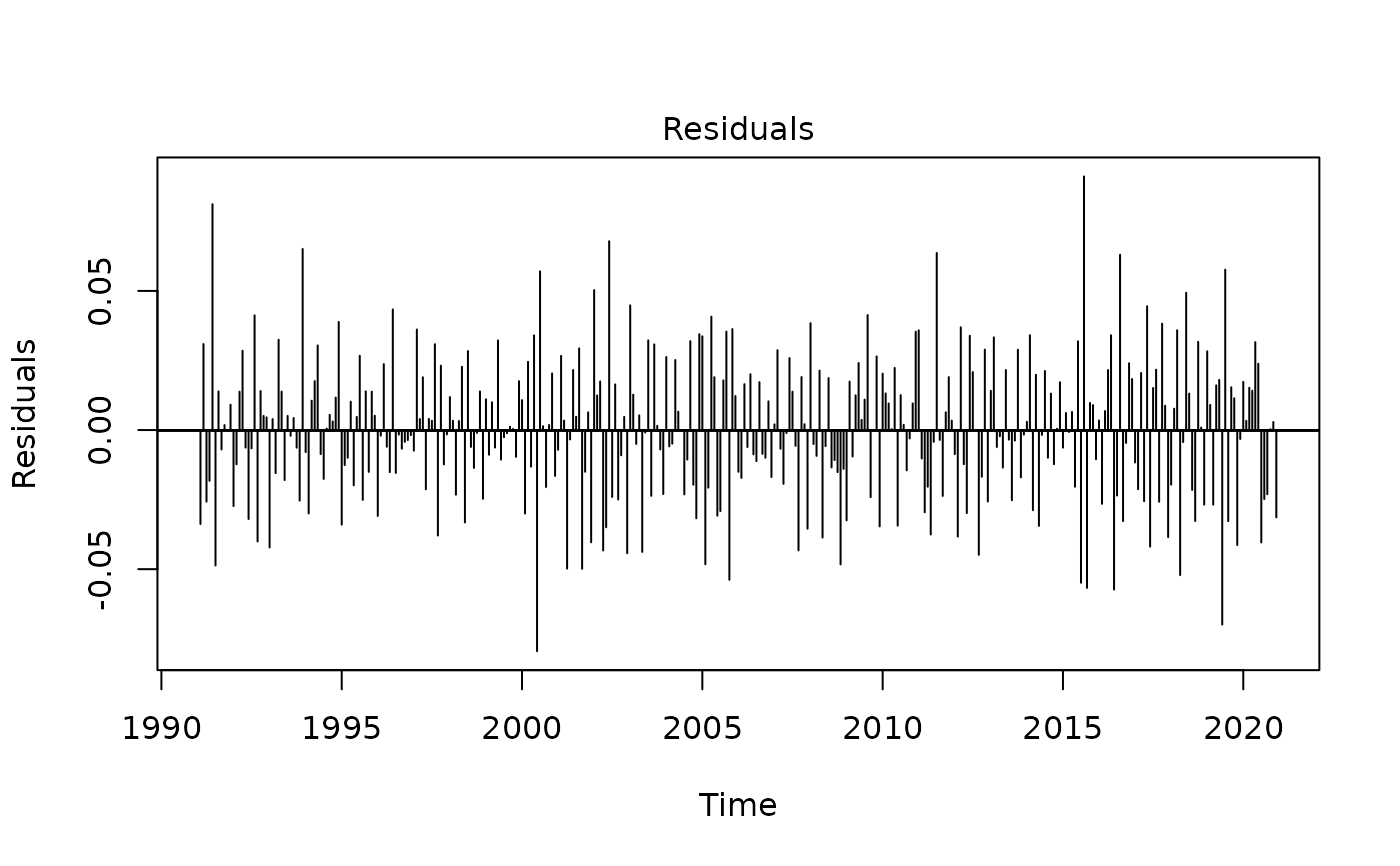

the residuals (time series). They can be also extracted with the function

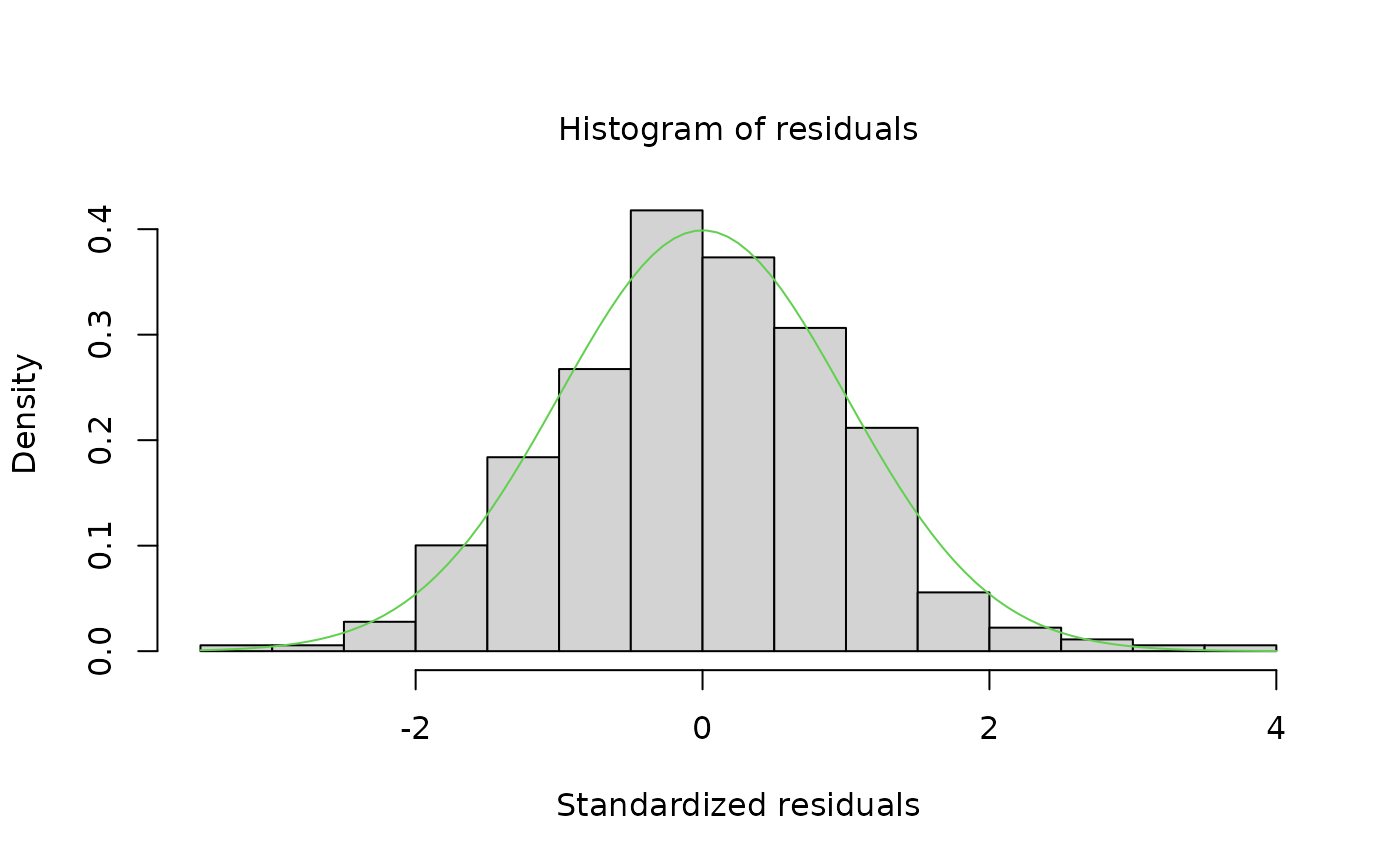

residuals.- residuals.stat

a list containing statistics on the RegARIMA residuals. It provides the residuals standard error (

st.error) and the results of normality, independence and linearity of the residuals (tests) - object of classc("regarima_rtests","data.frame").- forecast

a ts matrix containing the forecast of the original series (

fcst) and its standard error (fcsterr).

Details

When seasonally adjusting with X13 and TRAMO-SEATS, the first step consists in pre-adjusting the original series with a RegARIMA model, where the original series is corrected for any deterministic effects and missing observations. This step is also referred to as the linearization of the original series.

The RegARIMA model (model with ARIMA errors) is specified as such:

$$z_t = y_t\beta + x_t$$

where:

\(z_t\) is the original series;

\(\beta = (\beta_1,...,\beta_n)\) is a vector of regression coefficients;

\(y_t = (y_{1t},...,y_{nt})\) are \(n\) regression variables (outliers, calendar effects, user-defined variables);

\(x_t\) is a disturbance that follows the general ARIMA process: \(\phi(B)\delta(B)x_t = \theta(B)a_t\); where \(\phi(B), \delta(B)\) and \(\theta(B)\) are finite polynomials in \(B\) and \(a_t\) is a white noise variable with zero mean and a constant variance.

The polynomial \(\phi(B)\) is a stationary autoregressive (AR) polynomial in \(B\), which is a product of the stationary regular AR polynomial in \(B\) and the stationary seasonal polynomial in \(B^s\):

$$\phi(B)=\phi_p(B)\Phi_{bp}(B^s)=(1+\phi_1B+...+\phi_pB^p)(1+\Phi_1B^s+...+\Phi_{bp}B^{bps})$$

where:

\(p\) is the number of regular AR terms (here and in 'JDemetra+', \(p \le 3\));

\(bp\) is the number of seasonal AR terms (here and in 'JDemetra+', \(bp \le 1\));

\(s\) is the number of observations per year (ie. The time series frequency).

The polynomial \(\theta(B)\) is an invertible moving average (MA) polynomial in \(B\), which is a product of the invertible regular MA polynomial in \(B\) and the invertible seasonal MA polynomial in \(B^s\):

$$\theta(B)=\theta_q(B)\Theta_{bq}(B^s)=(1+\theta_1B+...+\theta_qB^q)(1+\Theta_1B^s+...+\Theta_{bq}B^{bqs})$$

where:

\(q\) is the number of regular MA terms (here and in 'JDemetra+', \(q \le 3\));

\(bq\) is the number of seasonal MA terms (here and in 'JDemetra+', \(bq \le 1\)).

The polynomial \(\delta(B)\) is the non-stationary AR polynomial in \(B\) (unit roots):

$$\delta(B) = (1-B)^d(1-B^s)^{d_s}$$

where:

\(d\) is the regular differencing order (here and in 'JDemetra+', \(d \le 1\));

\(d_s\) is the seasonal differencing order (here and in 'JDemetra+', \(d_s \le 1\)).

NB. The notations used for AR and MA processes, as well as the model denoted as ARIMA \((P,D,Q)(BP,BD,BQ)\), are consistent with those in 'JDemetra+'.

The available predefined 'JDemetra+' X13 and TRAMO-SEATS model specifications are described in the tables below:

X13:

| Identifier | | Log/level detection | | Outliers detection | | Calendar effects | | ARIMA | RG0 | | NA | |

| NA | | NA | | Airline(+mean) | RG1 | | automatic | | AO/LS/TC | | NA | |

| Airline(+mean) | RG2c | | automatic | | AO/LS/TC | | 2 td vars + Easter | | Airline(+mean) | RG3 | |

| automatic | | AO/LS/TC | | NA | | automatic | RG4c | | automatic | | AO/LS/TC | |

| 2 td vars + Easter | | automatic | RG5c | | automatic | | AO/LS/TC | | 7 td vars + Easter | | automatic |

TRAMO-SEATS:

| Identifier | | Log/level detection | | Outliers detection | | Calendar effects | | ARIMA | TR0 | | NA | | NA | |

| NA | | Airline(+mean) | TR1 | | automatic | | AO/LS/TC | | NA | | Airline(+mean) | TR2 | |

| automatic | | AO/LS/TC | | 2 td vars + Easter | | Airline(+mean) | TR3 | | automatic | | AO/LS/TC | | NA | |

| automatic | TR4 | | automatic | | AO/LS/TC | | 2 td vars + Easter | | automatic | TR5 | | automatic | |

| AO/LS/TC | | 7 td vars + Easter | | automatic | TRfull | | automatic | | AO/LS/TC | | automatic | | automatic |

References

More information and examples related to 'JDemetra+' features in the online documentation: https://jdemetra-new-documentation.netlify.app/

BOX G.E.P. and JENKINS G.M. (1970), "Time Series Analysis: Forecasting and Control", Holden-Day, San Francisco.

BOX G.E.P., JENKINS G.M., REINSEL G.C. and LJUNG G.M. (2015), "Time Series Analysis: Forecasting and Control", John Wiley & Sons, Hoboken, N. J., 5th edition.

Examples

# \donttest{

# X13 method

myseries <- ipi_c_eu[, "FR"]

myreg <- regarima_x13(myseries, spec ="RG5c")

summary(myreg)

#> y = regression model + arima (2, 1, 1, 0, 1, 1)

#>

#> Model: RegARIMA - X13

#> Estimation span: from 1-1990 to 12-2020

#> Log-transformation: no

#> Regression model: no mean, trading days effect(7), leap year effect, Easter effect, outliers(4)

#>

#> Coefficients:

#> ARIMA:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Phi(1) 0.0003269 0.1077296 0.003 0.9976

#> Phi(2) 0.1688192 0.0740996 2.278 0.0233 *

#> Theta(1) -0.5485606 0.1016550 -5.396 1.24e-07 ***

#> BTheta(1) -0.6660849 0.0422242 -15.775 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Regression model:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Monday 0.55932 0.22801 2.453 0.014638 *

#> Tuesday 0.88221 0.22832 3.864 0.000132 ***

#> Wednesday 1.03996 0.22930 4.535 7.85e-06 ***

#> Thursday 0.04943 0.22944 0.215 0.829549

#> Friday 0.91132 0.22988 3.964 8.88e-05 ***

#> Saturday -1.57769 0.22775 -6.927 1.99e-11 ***

#> Leap year 2.15403 0.70527 3.054 0.002425 **

#> Easter [1] -2.37950 0.45391 -5.242 2.71e-07 ***

#> TC (4-2020) -35.59245 2.17330 -16.377 < 2e-16 ***

#> AO (3-2020) -20.89026 2.18013 -9.582 < 2e-16 ***

#> AO (5-2011) 13.49850 1.85694 7.269 2.28e-12 ***

#> LS (11-2008) -12.54901 1.63554 -7.673 1.60e-13 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 2.218 on 342 degrees of freedom

#> Log likelihood = -799.1, aic = 1632, aicc = 1634, bic(corrected for length) = 1.855

#>

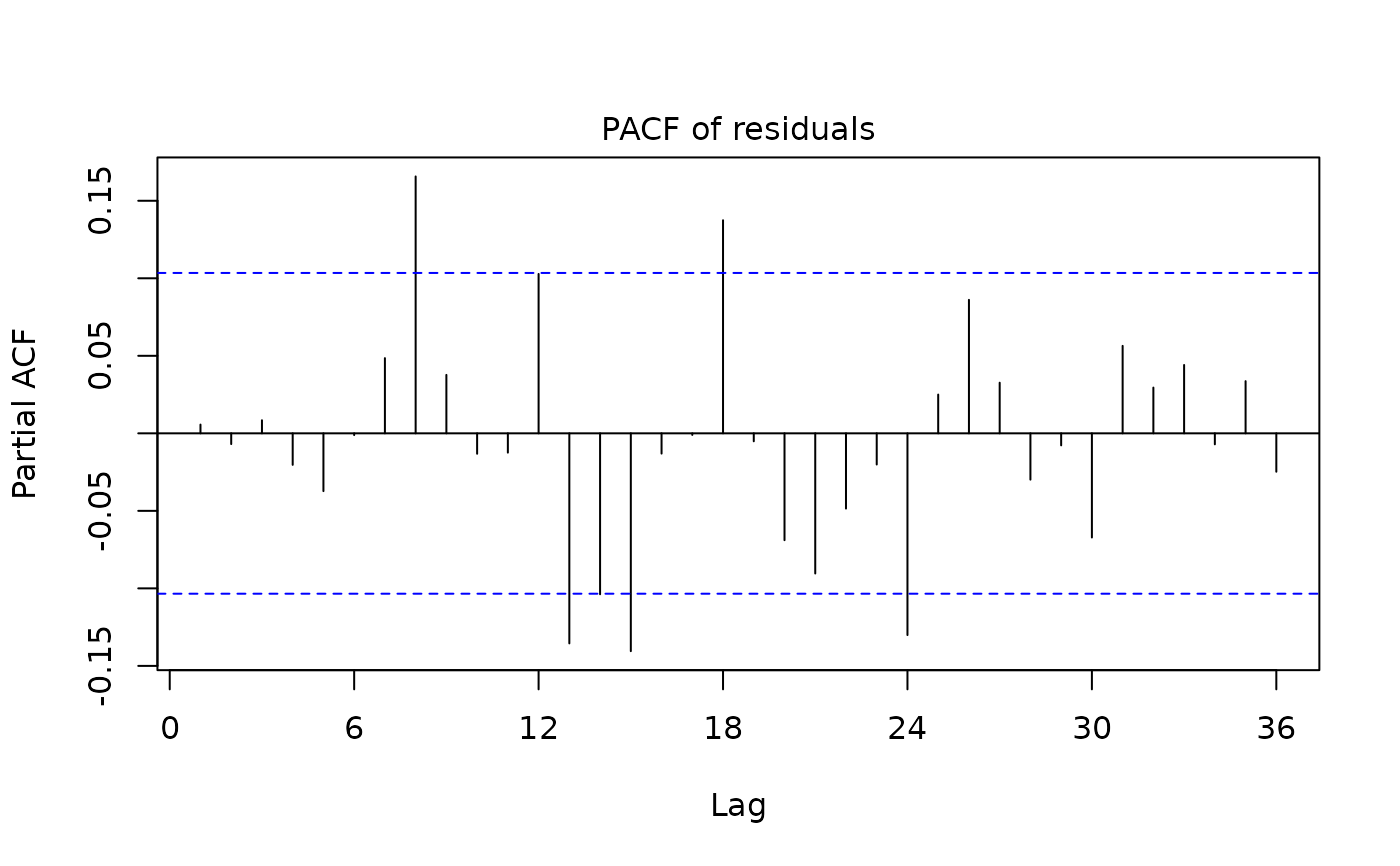

plot(myreg)

myspec1 <- regarima_spec_x13(myreg, tradingdays.option = "WorkingDays")

myreg1 <- regarima(myseries, myspec1)

myspec2 <- regarima_spec_x13(myreg, usrdef.outliersEnabled = TRUE,

usrdef.outliersType = c("LS", "AO"),

usrdef.outliersDate = c("2008-10-01", "2002-01-01"),

usrdef.outliersCoef = c(36, 14),

transform.function = "None")

myreg2 <- regarima(myseries, myspec2)

myreg2

#> y = regression model + arima (2, 1, 1, 0, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.07859 0.114

#> Phi(2) 0.19792 0.076

#> Theta(1) -0.48272 0.111

#> BTheta(1) -0.65916 0.043

#>

#> Estimate Std. Error

#> Monday 0.64094 0.228

#> Tuesday 0.81794 0.229

#> Wednesday 1.05374 0.229

#> Thursday 0.06981 0.228

#> Friday 0.93434 0.228

#> Saturday -1.63686 0.226

#> Leap year 2.11550 0.697

#> Easter [1] -2.38135 0.451

#> AO (9-2008) 31.95554 2.924

#> LS (9-2008) -57.04093 2.657

#> TC (4-2020) -35.62104 2.120

#> AO (3-2020) -21.00931 2.145

#> AO (5-2011) 13.21877 1.832

#> TC (9-2008) 23.44654 4.001

#> TC (12-2001) -20.47521 2.922

#> AO (12-2001) 17.13461 2.962

#> TC (2-2002) 10.61731 1.937

#>

#> Fixed outliers:

#> Coefficients

#> LS (10-2008) 36

#> AO (1-2002) 14

#>

#>

#> Residual standard error: 2.178 on 337 degrees of freedom

#> Log likelihood = -792.6, aic = 1629 aicc = 1632, bic(corrected for length) = 1.901

#>

myspec3 <- regarima_spec_x13(myreg, automdl.enabled = FALSE,

arima.p = 1, arima.q = 1,

arima.bp = 0, arima.bq = 1,

arima.coefEnabled = TRUE,

arima.coef = c(-0.8, -0.6, 0),

arima.coefType = c(rep("Fixed", 2), "Undefined"))

s_arimaCoef(myspec3)

#> Type Value

#> Phi(1) Fixed -0.8

#> Theta(1) Fixed -0.6

#> BTheta(1) Undefined 0.0

myreg3 <- regarima(myseries, myspec3)

summary(myreg3)

#> y = regression model + arima (1, 1, 1, 0, 1, 1)

#>

#> Model: RegARIMA - X13

#> Estimation span: from 1-1990 to 12-2020

#> Log-transformation: yes

#> Regression model: no mean, trading days effect(6), no leap year effect, Easter effect, outliers(3)

#>

#> Coefficients:

#> ARIMA:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Phi(1) -0.8000 0.0000 NA NA

#> Theta(1) -0.6000 0.0000 NA NA

#> BTheta(1) -0.6977 0.0399 -17.49 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Regression model:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Monday 0.006317 0.001791 3.526 0.000476 ***

#> Tuesday 0.007824 0.001793 4.363 1.68e-05 ***

#> Wednesday 0.010528 0.001802 5.841 1.16e-08 ***

#> Thursday 0.001857 0.001811 1.025 0.306022

#> Friday 0.010099 0.001812 5.574 4.90e-08 ***

#> Saturday -0.018439 0.001781 -10.354 < 2e-16 ***

#> Easter [1] -0.020593 0.003515 -5.859 1.06e-08 ***

#> TC (4-2020) -0.475720 0.031229 -15.233 < 2e-16 ***

#> AO (3-2020) -0.213355 0.023246 -9.178 < 2e-16 ***

#> AO (5-2011) 0.143705 0.015529 9.254 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.0256 on 347 degrees of freedom

#> Log likelihood = 802.3, aic = 1733, aicc = 1734, bic(corrected for length) = -7.15

#>

plot(myreg3)

myspec1 <- regarima_spec_x13(myreg, tradingdays.option = "WorkingDays")

myreg1 <- regarima(myseries, myspec1)

myspec2 <- regarima_spec_x13(myreg, usrdef.outliersEnabled = TRUE,

usrdef.outliersType = c("LS", "AO"),

usrdef.outliersDate = c("2008-10-01", "2002-01-01"),

usrdef.outliersCoef = c(36, 14),

transform.function = "None")

myreg2 <- regarima(myseries, myspec2)

myreg2

#> y = regression model + arima (2, 1, 1, 0, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.07859 0.114

#> Phi(2) 0.19792 0.076

#> Theta(1) -0.48272 0.111

#> BTheta(1) -0.65916 0.043

#>

#> Estimate Std. Error

#> Monday 0.64094 0.228

#> Tuesday 0.81794 0.229

#> Wednesday 1.05374 0.229

#> Thursday 0.06981 0.228

#> Friday 0.93434 0.228

#> Saturday -1.63686 0.226

#> Leap year 2.11550 0.697

#> Easter [1] -2.38135 0.451

#> AO (9-2008) 31.95554 2.924

#> LS (9-2008) -57.04093 2.657

#> TC (4-2020) -35.62104 2.120

#> AO (3-2020) -21.00931 2.145

#> AO (5-2011) 13.21877 1.832

#> TC (9-2008) 23.44654 4.001

#> TC (12-2001) -20.47521 2.922

#> AO (12-2001) 17.13461 2.962

#> TC (2-2002) 10.61731 1.937

#>

#> Fixed outliers:

#> Coefficients

#> LS (10-2008) 36

#> AO (1-2002) 14

#>

#>

#> Residual standard error: 2.178 on 337 degrees of freedom

#> Log likelihood = -792.6, aic = 1629 aicc = 1632, bic(corrected for length) = 1.901

#>

myspec3 <- regarima_spec_x13(myreg, automdl.enabled = FALSE,

arima.p = 1, arima.q = 1,

arima.bp = 0, arima.bq = 1,

arima.coefEnabled = TRUE,

arima.coef = c(-0.8, -0.6, 0),

arima.coefType = c(rep("Fixed", 2), "Undefined"))

s_arimaCoef(myspec3)

#> Type Value

#> Phi(1) Fixed -0.8

#> Theta(1) Fixed -0.6

#> BTheta(1) Undefined 0.0

myreg3 <- regarima(myseries, myspec3)

summary(myreg3)

#> y = regression model + arima (1, 1, 1, 0, 1, 1)

#>

#> Model: RegARIMA - X13

#> Estimation span: from 1-1990 to 12-2020

#> Log-transformation: yes

#> Regression model: no mean, trading days effect(6), no leap year effect, Easter effect, outliers(3)

#>

#> Coefficients:

#> ARIMA:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Phi(1) -0.8000 0.0000 NA NA

#> Theta(1) -0.6000 0.0000 NA NA

#> BTheta(1) -0.6977 0.0399 -17.49 <2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#> Regression model:

#> Estimate Std. Error T-stat Pr(>|t|)

#> Monday 0.006317 0.001791 3.526 0.000476 ***

#> Tuesday 0.007824 0.001793 4.363 1.68e-05 ***

#> Wednesday 0.010528 0.001802 5.841 1.16e-08 ***

#> Thursday 0.001857 0.001811 1.025 0.306022

#> Friday 0.010099 0.001812 5.574 4.90e-08 ***

#> Saturday -0.018439 0.001781 -10.354 < 2e-16 ***

#> Easter [1] -0.020593 0.003515 -5.859 1.06e-08 ***

#> TC (4-2020) -0.475720 0.031229 -15.233 < 2e-16 ***

#> AO (3-2020) -0.213355 0.023246 -9.178 < 2e-16 ***

#> AO (5-2011) 0.143705 0.015529 9.254 < 2e-16 ***

#> ---

#> Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

#>

#>

#> Residual standard error: 0.0256 on 347 degrees of freedom

#> Log likelihood = 802.3, aic = 1733, aicc = 1734, bic(corrected for length) = -7.15

#>

plot(myreg3)

# TRAMO-SEATS method

myspec <- regarima_spec_tramoseats("TRfull")

myreg <- regarima(myseries, myspec)

myreg

#> y = regression model + arima (2, 1, 0, 0, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.4032 0.051

#> Phi(2) 0.2883 0.051

#> BTheta(1) -0.6641 0.042

#>

#> Estimate Std. Error

#> Week days 0.6994 0.032

#> Leap year 2.3231 0.690

#> Easter [6] -2.5154 0.436

#> AO (5-2011) 13.4679 1.787

#> TC (4-2020) -22.2128 2.205

#> TC (3-2020) -21.0391 2.217

#> AO (5-2000) 6.7386 1.794

#>

#>

#> Residual standard error: 2.326 on 348 degrees of freedom

#> Log likelihood = -816.1, aic = 1654 aicc = 1655, bic(corrected for length) = 1.852

#>

myspec2 <- regarima_spec_tramoseats(myspec, tradingdays.mauto = "Unused",

tradingdays.option = "WorkingDays",

easter.type = "Standard",

automdl.enabled = FALSE, arima.mu = TRUE)

myreg2 <- regarima(myseries, myspec2)

var1 <- ts(rnorm(length(myseries))*10, start = start(myseries), frequency = 12)

var2 <- ts(rnorm(length(myseries))*100, start = start(myseries), frequency = 12)

var <- ts.union(var1, var2)

myspec3 <- regarima_spec_tramoseats(myspec,

usrdef.varEnabled = TRUE, usrdef.var = var)

s_preVar(myspec3)

#> $series

#> var1 var2

#> Jan 1990 -16.30989402 2.0831228

#> Feb 1990 5.12426950 0.7586777

#> Mar 1990 -18.63011492 93.0844030

#> Apr 1990 -5.22012515 -68.4749941

#> May 1990 -0.52601910 33.7401513

#> Jun 1990 5.42996343 -41.2137704

#> Jul 1990 -9.14074827 93.4261130

#> Aug 1990 4.68154420 184.0316741

#> Sep 1990 3.62951256 -70.4819663

#> Oct 1990 -13.04543545 0.8510312

#> Nov 1990 7.37776321 203.4189886

#> Dec 1990 18.88504929 -134.1686068

#> Jan 1991 -0.97445104 115.8979182

#> Feb 1991 -9.35847354 -20.3208958

#> Mar 1991 -0.15950311 -37.8028555

#> Apr 1991 -8.26788954 173.6111043

#> May 1991 -15.12399651 -84.5247816

#> Jun 1991 9.35363190 -96.1571493

#> Jul 1991 1.76488611 101.7491053

#> Aug 1991 2.43685465 -149.6053742

#> Sep 1991 16.23548883 -118.4818730

#> Oct 1991 1.12038083 63.0234373

#> Nov 1991 -1.33997013 210.1252514

#> Dec 1991 -19.10087468 -61.3736810

#> Jan 1992 -2.79237242 -163.4638272

#> Feb 1992 -3.13445978 -1.0441117

#> Mar 1992 10.67307879 -65.6506139

#> Apr 1992 0.70034850 -66.9533441

#> May 1992 -6.39123324 -47.8589028

#> Jun 1992 -0.49964899 131.9456316

#> Jul 1992 -2.51483443 63.6562761

#> Aug 1992 4.44797116 51.4327782

#> Sep 1992 27.55417575 -175.1375113

#> Oct 1992 0.46531380 89.3597518

#> Nov 1992 5.77709069 22.3038372

#> Dec 1992 1.18194874 58.0816593

#> Jan 1993 -19.11720491 -17.7821421

#> Feb 1993 8.62086482 74.0966708

#> Mar 1993 -2.43236740 -99.7443079

#> Apr 1993 -2.06087195 -293.8977561

#> May 1993 0.19177592 71.9015661

#> Jun 1993 0.29560754 -69.8005041

#> Jul 1993 5.49827542 -189.4125843

#> Aug 1993 -22.74114857 7.6299249

#> Sep 1993 26.82557184 87.5308501

#> Oct 1993 -3.61221255 45.3827393

#> Nov 1993 2.13355750 -85.0716906

#> Dec 1993 10.74345882 56.6201613

#> Jan 1994 -6.65088249 115.2211954

#> Feb 1994 11.13952419 -75.6197377

#> Mar 1994 -2.45896412 -48.9258334

#> Apr 1994 -11.77563309 -116.6052337

#> May 1994 -9.75850616 -47.9668950

#> Jun 1994 10.65057320 11.5348218

#> Jul 1994 1.31670635 -176.8048407

#> Aug 1994 4.88628809 -140.7638919

#> Sep 1994 -16.99450568 70.9178461

#> Oct 1994 -14.70736306 -124.0842940

#> Nov 1994 2.84150344 -36.8327348

#> Dec 1994 13.37320413 46.2080093

#> Jan 1995 2.36696283 -32.2833101

#> Feb 1995 13.18293384 -128.7214810

#> Mar 1995 5.23909788 -103.0040247

#> Apr 1995 6.06748047 151.4089316

#> May 1995 -1.09935672 34.6903586

#> Jun 1995 1.72181715 177.9441542

#> Jul 1995 -0.90327287 38.6630924

#> Aug 1995 19.24343341 -91.8695239

#> Sep 1995 12.98392759 -158.4336488

#> Oct 1995 7.48791268 -8.4058892

#> Nov 1995 5.56224329 -208.5070889

#> Dec 1995 -5.48257264 0.3567992

#> Jan 1996 11.10534893 -35.5770822

#> Feb 1996 -26.12334333 114.6359751

#> Mar 1996 -1.55693776 -22.1188446

#> Apr 1996 4.33889790 101.8179021

#> May 1996 -3.81951112 -26.3719295

#> Jun 1996 4.24187575 165.8542305

#> Jul 1996 10.63101996 -77.4086771

#> Aug 1996 10.48712620 -92.3937880

#> Sep 1996 -0.38102895 -27.5533378

#> Oct 1996 4.86148920 -59.3399688

#> Nov 1996 16.72882611 -12.2285891

#> Dec 1996 -3.54361164 117.9784246

#> Jan 1997 9.46347886 64.1037374

#> Feb 1997 13.16826356 -62.9588508

#> Mar 1997 -2.96640025 -80.7734971

#> Apr 1997 -3.87213575 -86.0489929

#> May 1997 -7.85432656 -216.9238693

#> Jun 1997 -10.56736867 -137.5836518

#> Jul 1997 -7.95541430 -49.3132472

#> Aug 1997 -17.56275428 -58.1652027

#> Sep 1997 -6.90537897 -16.7229304

#> Oct 1997 -5.58541994 48.5993129

#> Nov 1997 -5.36663326 -133.3395796

#> Dec 1997 2.27127133 -26.1965625

#> Jan 1998 9.78454920 65.2386303

#> Feb 1998 -2.08882651 74.8854971

#> Mar 1998 -13.99410460 89.6560285

#> Apr 1998 2.58537288 148.9300424

#> May 1998 -4.41799453 -65.9403481

#> Jun 1998 5.68599861 53.7283179

#> Jul 1998 21.26850459 74.6803067

#> Aug 1998 4.24858441 189.6317084

#> Sep 1998 -16.84281532 -206.0070725

#> Oct 1998 2.49401784 6.4543870

#> Nov 1998 10.72838252 -26.5147403

#> Dec 1998 20.39369263 -44.7344531

#> Jan 1999 4.49453778 -141.0700927

#> Feb 1999 13.91814046 -50.6418882

#> Mar 1999 4.26566547 -26.9761838

#> Apr 1999 1.07583992 -108.5154918

#> May 1999 0.22294733 36.2159127

#> Jun 1999 6.03611011 -33.5672143

#> Jul 1999 -2.62650573 136.3804498

#> Aug 1999 -5.28264082 -71.1524136

#> Sep 1999 1.92149422 66.2178797

#> Oct 1999 -11.46199669 29.1130223

#> Nov 1999 8.46184665 19.7958000

#> Dec 1999 0.81719629 -120.3566106

#> Jan 2000 -13.05117010 -3.9817044

#> Feb 2000 -9.44912060 68.6982465

#> Mar 2000 4.54341594 70.5267007

#> Apr 2000 -8.55202501 99.1441680

#> May 2000 -2.86895219 114.4248971

#> Jun 2000 8.94961626 -123.8910243

#> Jul 2000 0.67304440 265.4898333

#> Aug 2000 -1.62676337 -15.6917189

#> Sep 2000 -8.27310169 -42.3490117

#> Oct 2000 18.76505621 -19.8387058

#> Nov 2000 7.66440199 -89.4802407

#> Dec 2000 9.79956696 90.4269119

#> Jan 2001 13.21780992 7.9649210

#> Feb 2001 -11.19710829 -125.8827223

#> Mar 2001 5.14599819 102.5685106

#> Apr 2001 -15.09099836 -73.0778603

#> May 2001 15.32741480 -19.0145507

#> Jun 2001 4.29147371 52.8864693

#> Jul 2001 1.22103414 55.0210535

#> Aug 2001 -11.38012401 54.9684337

#> Sep 2001 -5.58015129 -65.9542372

#> Oct 2001 10.52538537 5.7421706

#> Nov 2001 6.77683644 -280.8010508

#> Dec 2001 0.38499547 -91.2259753

#> Jan 2002 -3.56381187 -78.2379163

#> Feb 2002 7.82844102 -66.4104924

#> Mar 2002 8.04411616 62.6309770

#> Apr 2002 -19.00060823 -50.7248206

#> May 2002 9.35784286 27.0361335

#> Jun 2002 -3.09051503 46.7476865

#> Jul 2002 2.63066677 72.3994958

#> Aug 2002 -17.90591856 61.3836939

#> Sep 2002 -7.88258845 -61.7869202

#> Oct 2002 -11.33021669 22.0724902

#> Nov 2002 3.63652568 112.7926598

#> Dec 2002 -2.85887914 181.3454336

#> Jan 2003 5.17669134 -8.3825685

#> Feb 2003 -1.02908670 136.7706666

#> Mar 2003 -9.74069593 -62.7434620

#> Apr 2003 12.70672301 -21.6629150

#> May 2003 9.60864787 -68.3713824

#> Jun 2003 7.68721370 -44.4702734

#> Jul 2003 10.35930771 60.6489806

#> Aug 2003 -4.73887074 62.4183075

#> Sep 2003 -12.75334875 -69.5431074

#> Oct 2003 -3.05620674 -78.3639078

#> Nov 2003 22.11769487 -95.3123859

#> Dec 2003 -10.41668381 179.2756071

#> Jan 2004 -11.46523850 34.8976696

#> Feb 2004 -16.75327303 25.9103768

#> Mar 2004 15.25938655 -80.5951897

#> Apr 2004 5.54185515 10.5664701

#> May 2004 19.93110265 -33.3599682

#> Jun 2004 -1.54120740 164.1847970

#> Jul 2004 25.64408338 -64.3905859

#> Aug 2004 10.61999145 58.7020562

#> Sep 2004 11.42694878 -15.0403088

#> Oct 2004 11.23838843 -171.0821848

#> Nov 2004 -3.97001493 143.1032558

#> Dec 2004 -8.23261151 -264.5212268

#> Jan 2005 -5.78884625 -103.2457405

#> Feb 2005 17.63789378 -70.7466431

#> Mar 2005 1.32992146 -70.0560014

#> Apr 2005 3.76499328 53.7885439

#> May 2005 11.38707653 -31.6332175

#> Jun 2005 12.41263075 -83.9622754

#> Jul 2005 6.12090945 -135.4928062

#> Aug 2005 -4.29380087 -81.7568272

#> Sep 2005 13.60461327 -63.4400003

#> Oct 2005 -0.70857431 81.5949433

#> Nov 2005 -2.72153684 30.2795706

#> Dec 2005 -24.46680029 180.7086625

#> Jan 2006 0.65486641 -89.4026756

#> Feb 2006 -10.98508902 -4.6428211

#> Mar 2006 -6.33178176 -47.1179138

#> Apr 2006 -20.63654451 -52.6692630

#> May 2006 26.48932029 -9.5134908

#> Jun 2006 -11.53398386 -249.5364809

#> Jul 2006 -3.40637876 16.6889217

#> Aug 2006 7.86362576 35.0492384

#> Sep 2006 -12.70513110 143.3701009

#> Oct 2006 5.42141549 76.5906803

#> Nov 2006 0.75105900 116.7520670

#> Dec 2006 5.58514422 -13.6943429

#> Jan 2007 4.15406399 -51.4902044

#> Feb 2007 -14.52299769 151.9744468

#> Mar 2007 9.41206122 -32.8491678

#> Apr 2007 -3.38935872 -5.3671506

#> May 2007 -0.75574247 -56.3524635

#> Jun 2007 0.40204392 -74.3908963

#> Jul 2007 1.24301066 -10.9041651

#> Aug 2007 -9.98432551 -56.0829227

#> Sep 2007 12.33390065 18.8001549

#> Oct 2007 3.40424488 74.8850942

#> Nov 2007 -4.72702482 -191.6538316

#> Dec 2007 7.08753061 23.6095847

#> Jan 2008 -15.28958715 62.8953415

#> Feb 2008 2.37425345 41.7925676

#> Mar 2008 -13.12814246 197.6758477

#> Apr 2008 7.47028587 -50.6286298

#> May 2008 -15.62518435 -110.9968853

#> Jun 2008 0.71053360 -94.8705723

#> Jul 2008 -6.39534770 47.6843757

#> Aug 2008 -8.45195739 -79.5201560

#> Sep 2008 6.75244698 23.4326923

#> Oct 2008 11.53375794 -122.2451097

#> Nov 2008 -16.86504742 -245.3647354

#> Dec 2008 -9.02814949 -148.9260814

#> Jan 2009 13.17633698 -43.2147734

#> Feb 2009 11.00189745 -94.2554006

#> Mar 2009 12.03767839 -12.1450799

#> Apr 2009 -14.31270777 133.6446798

#> May 2009 13.82910861 -86.0356182

#> Jun 2009 0.03125940 66.6537820

#> Jul 2009 -0.77886824 -142.1534746

#> Aug 2009 4.41428226 117.0056168

#> Sep 2009 1.28922896 -140.4714543

#> Oct 2009 -8.30214260 110.1708096

#> Nov 2009 -5.03592910 69.7986263

#> Dec 2009 -11.93641182 -86.4349803

#> Jan 2010 -7.51723323 -109.1470351

#> Feb 2010 14.55841403 -3.7051465

#> Mar 2010 -8.28603533 81.0053792

#> Apr 2010 2.89774460 -49.9355412

#> May 2010 -4.80053484 94.8031588

#> Jun 2010 -6.04829354 -17.4245957

#> Jul 2010 14.60110180 -110.6235952

#> Aug 2010 1.49679354 -94.5985005

#> Sep 2010 -14.33321100 28.9089591

#> Oct 2010 -0.10303319 87.6913145

#> Nov 2010 -2.12236035 -114.8903940

#> Dec 2010 -9.06340179 -113.7612756

#> Jan 2011 -21.02152479 -143.7246735

#> Feb 2011 18.93360464 -49.4143476

#> Mar 2011 -9.68125837 84.0801808

#> Apr 2011 -1.02603036 79.1534124

#> May 2011 2.39959572 -16.8848948

#> Jun 2011 0.60898893 61.2722104

#> Jul 2011 -21.77576028 -77.1158924

#> Aug 2011 -1.17860143 88.8628993

#> Sep 2011 1.12294787 1.3214477

#> Oct 2011 0.07886198 22.5339515

#> Nov 2011 18.77743872 -72.9915210

#> Dec 2011 21.58756554 -122.2487070

#> Jan 2012 7.09714522 40.6805171

#> Feb 2012 7.66983379 -75.1012223

#> Mar 2012 -3.08211421 -16.2116540

#> Apr 2012 10.12001849 35.2010126

#> May 2012 -9.19051597 -28.9058300

#> Jun 2012 5.63380077 10.4662227

#> Jul 2012 3.22482749 72.0186531

#> Aug 2012 3.66674363 -61.1046082

#> Sep 2012 11.29835153 -110.6914072

#> Oct 2012 -9.41498076 53.4803326

#> Nov 2012 2.17837643 73.6067968

#> Dec 2012 14.15412293 -122.2501574

#> Jan 2013 -3.83733048 102.1415310

#> Feb 2013 -1.74086374 46.5165158

#> Mar 2013 -2.21744517 79.0472705

#> Apr 2013 -10.09528722 -13.0264801

#> May 2013 4.80725266 -93.0285334

#> Jun 2013 16.04407328 -36.4851004

#> Jul 2013 -15.15024529 15.3872493

#> Aug 2013 -14.16023914 41.3154818

#> Sep 2013 8.76777327 248.0823360

#> Oct 2013 6.24132413 -217.9956742

#> Nov 2013 21.12277288 42.0874578

#> Dec 2013 -3.56124416 -35.7528325

#> Jan 2014 -10.64464209 -64.6861514

#> Feb 2014 10.77116538 -5.0141801

#> Mar 2014 11.81575567 41.6942847

#> Apr 2014 1.98392095 -63.2587542

#> May 2014 -4.00405249 115.0146673

#> Jun 2014 6.16154281 -23.5475907

#> Jul 2014 19.74156748 -164.3107386

#> Aug 2014 18.84662324 -150.3382146

#> Sep 2014 -15.88620547 -205.0584847

#> Oct 2014 -5.39923164 -75.3198229

#> Nov 2014 -11.69461464 -13.4141958

#> Dec 2014 5.59105989 100.5782847

#> Jan 2015 -18.19347247 216.7186798

#> Feb 2015 3.93343972 232.2556540

#> Mar 2015 0.42134106 -102.0423391

#> Apr 2015 11.79664177 4.8814436

#> May 2015 -2.56921176 -77.1888628

#> Jun 2015 -10.56336098 -78.5235068

#> Jul 2015 1.98777205 -72.6603031

#> Aug 2015 6.50533552 68.1878032

#> Sep 2015 3.43913337 -22.9843287

#> Oct 2015 14.77532312 -151.0601724

#> Nov 2015 0.72025698 -58.3727687

#> Dec 2015 21.26444534 -202.2918454

#> Jan 2016 -14.76196906 40.3504676

#> Feb 2016 4.07888500 55.0015549

#> Mar 2016 13.93977798 2.8357122

#> Apr 2016 3.60278296 89.3165020

#> May 2016 6.54550251 -37.6555496

#> Jun 2016 10.52155422 60.5884808

#> Jul 2016 -19.79555125 -0.4874726

#> Aug 2016 12.08385605 -52.0796373

#> Sep 2016 -1.69280084 -63.9018598

#> Oct 2016 2.95029753 -63.5894137

#> Nov 2016 12.66340587 10.6586975

#> Dec 2016 -11.35343257 117.6914248

#> Jan 2017 -11.31053798 44.7391153

#> Feb 2017 1.09993384 227.2954766

#> Mar 2017 8.52905410 13.6058206

#> Apr 2017 -2.34337862 -199.9039133

#> May 2017 20.86688567 -42.0500870

#> Jun 2017 -1.10919371 -37.8407395

#> Jul 2017 -13.92847056 122.0774789

#> Aug 2017 -11.42290768 -154.1030292

#> Sep 2017 17.04608737 -31.0310122

#> Oct 2017 -0.80073634 -2.0108184

#> Nov 2017 -4.37281240 -239.0200336

#> Dec 2017 -1.19215094 88.9865359

#> Jan 2018 7.86462865 -148.2813325

#> Feb 2018 -5.78945246 44.5750348

#> Mar 2018 -1.45426885 136.9775856

#> Apr 2018 5.26457991 -2.0110027

#> May 2018 17.33578110 -10.9217587

#> Jun 2018 14.48657220 26.4661745

#> Jul 2018 15.18193149 30.3848264

#> Aug 2018 -3.84007254 -18.3388483

#> Sep 2018 18.27125177 55.9649672

#> Oct 2018 -5.51491750 -18.6553842

#> Nov 2018 -8.65753541 -81.2275372

#> Dec 2018 -3.43831481 -164.0581672

#> Jan 2019 10.62876458 50.7922478

#> Feb 2019 8.13058204 175.4336961

#> Mar 2019 18.03483361 59.2400202

#> Apr 2019 -1.05068694 101.6713288

#> May 2019 9.82453362 12.1620586

#> Jun 2019 -17.13302622 -107.8067265

#> Jul 2019 -8.32019527 -114.3565720

#> Aug 2019 11.00491882 -52.9643677

#> Sep 2019 -1.73820106 -68.1273156

#> Oct 2019 1.78812018 -20.2447559

#> Nov 2019 -6.98429449 168.4495721

#> Dec 2019 -9.60449159 -103.3773237

#> Jan 2020 -9.75423042 -15.5976673

#> Feb 2020 -3.38576503 -4.6400637

#> Mar 2020 11.52347074 -95.3628727

#> Apr 2020 4.05101183 41.6260798

#> May 2020 -4.70922497 11.4029609

#> Jun 2020 -1.33251019 6.3918753

#> Jul 2020 12.26682356 -91.9332238

#> Aug 2020 3.32943995 90.1335290

#> Sep 2020 -3.47088466 -79.7728297

#> Oct 2020 -0.98550690 66.8221204

#> Nov 2020 0.34766060 15.5214296

#> Dec 2020 3.86127022 12.8688092

#>

#> $description

#> type coeff

#> var1 Undefined NA

#> var2 Undefined NA

#>

myreg3 <- regarima(myseries, myspec3)

myreg3

#> y = regression model + arima (2, 1, 0, 1, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.4744 0.051

#> Phi(2) 0.3312 0.051

#> BPhi(1) -0.2569 0.072

#> BTheta(1) -0.8066 0.043

#>

#> Estimate Std. Error

#> r.var1 0.016274 0.009

#> r.var2 0.001222 0.001

#> Week days 0.689237 0.036

#> Leap year 2.054858 0.662

#> Easter [6] -2.509781 0.411

#> TC (4-2020) -22.552758 2.120

#> TC (3-2020) -21.119937 2.128

#> AO (5-2011) 12.809939 1.739

#> LS (1-2009) -9.611835 1.796

#>

#>

#> Residual standard error: 2.244 on 345 degrees of freedom

#> Log likelihood = -803.6, aic = 1635 aicc = 1636, bic(corrected for length) = 1.829

#>

# }

# TRAMO-SEATS method

myspec <- regarima_spec_tramoseats("TRfull")

myreg <- regarima(myseries, myspec)

myreg

#> y = regression model + arima (2, 1, 0, 0, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.4032 0.051

#> Phi(2) 0.2883 0.051

#> BTheta(1) -0.6641 0.042

#>

#> Estimate Std. Error

#> Week days 0.6994 0.032

#> Leap year 2.3231 0.690

#> Easter [6] -2.5154 0.436

#> AO (5-2011) 13.4679 1.787

#> TC (4-2020) -22.2128 2.205

#> TC (3-2020) -21.0391 2.217

#> AO (5-2000) 6.7386 1.794

#>

#>

#> Residual standard error: 2.326 on 348 degrees of freedom

#> Log likelihood = -816.1, aic = 1654 aicc = 1655, bic(corrected for length) = 1.852

#>

myspec2 <- regarima_spec_tramoseats(myspec, tradingdays.mauto = "Unused",

tradingdays.option = "WorkingDays",

easter.type = "Standard",

automdl.enabled = FALSE, arima.mu = TRUE)

myreg2 <- regarima(myseries, myspec2)

var1 <- ts(rnorm(length(myseries))*10, start = start(myseries), frequency = 12)

var2 <- ts(rnorm(length(myseries))*100, start = start(myseries), frequency = 12)

var <- ts.union(var1, var2)

myspec3 <- regarima_spec_tramoseats(myspec,

usrdef.varEnabled = TRUE, usrdef.var = var)

s_preVar(myspec3)

#> $series

#> var1 var2

#> Jan 1990 -16.30989402 2.0831228

#> Feb 1990 5.12426950 0.7586777

#> Mar 1990 -18.63011492 93.0844030

#> Apr 1990 -5.22012515 -68.4749941

#> May 1990 -0.52601910 33.7401513

#> Jun 1990 5.42996343 -41.2137704

#> Jul 1990 -9.14074827 93.4261130

#> Aug 1990 4.68154420 184.0316741

#> Sep 1990 3.62951256 -70.4819663

#> Oct 1990 -13.04543545 0.8510312

#> Nov 1990 7.37776321 203.4189886

#> Dec 1990 18.88504929 -134.1686068

#> Jan 1991 -0.97445104 115.8979182

#> Feb 1991 -9.35847354 -20.3208958

#> Mar 1991 -0.15950311 -37.8028555

#> Apr 1991 -8.26788954 173.6111043

#> May 1991 -15.12399651 -84.5247816

#> Jun 1991 9.35363190 -96.1571493

#> Jul 1991 1.76488611 101.7491053

#> Aug 1991 2.43685465 -149.6053742

#> Sep 1991 16.23548883 -118.4818730

#> Oct 1991 1.12038083 63.0234373

#> Nov 1991 -1.33997013 210.1252514

#> Dec 1991 -19.10087468 -61.3736810

#> Jan 1992 -2.79237242 -163.4638272

#> Feb 1992 -3.13445978 -1.0441117

#> Mar 1992 10.67307879 -65.6506139

#> Apr 1992 0.70034850 -66.9533441

#> May 1992 -6.39123324 -47.8589028

#> Jun 1992 -0.49964899 131.9456316

#> Jul 1992 -2.51483443 63.6562761

#> Aug 1992 4.44797116 51.4327782

#> Sep 1992 27.55417575 -175.1375113

#> Oct 1992 0.46531380 89.3597518

#> Nov 1992 5.77709069 22.3038372

#> Dec 1992 1.18194874 58.0816593

#> Jan 1993 -19.11720491 -17.7821421

#> Feb 1993 8.62086482 74.0966708

#> Mar 1993 -2.43236740 -99.7443079

#> Apr 1993 -2.06087195 -293.8977561

#> May 1993 0.19177592 71.9015661

#> Jun 1993 0.29560754 -69.8005041

#> Jul 1993 5.49827542 -189.4125843

#> Aug 1993 -22.74114857 7.6299249

#> Sep 1993 26.82557184 87.5308501

#> Oct 1993 -3.61221255 45.3827393

#> Nov 1993 2.13355750 -85.0716906

#> Dec 1993 10.74345882 56.6201613

#> Jan 1994 -6.65088249 115.2211954

#> Feb 1994 11.13952419 -75.6197377

#> Mar 1994 -2.45896412 -48.9258334

#> Apr 1994 -11.77563309 -116.6052337

#> May 1994 -9.75850616 -47.9668950

#> Jun 1994 10.65057320 11.5348218

#> Jul 1994 1.31670635 -176.8048407

#> Aug 1994 4.88628809 -140.7638919

#> Sep 1994 -16.99450568 70.9178461

#> Oct 1994 -14.70736306 -124.0842940

#> Nov 1994 2.84150344 -36.8327348

#> Dec 1994 13.37320413 46.2080093

#> Jan 1995 2.36696283 -32.2833101

#> Feb 1995 13.18293384 -128.7214810

#> Mar 1995 5.23909788 -103.0040247

#> Apr 1995 6.06748047 151.4089316

#> May 1995 -1.09935672 34.6903586

#> Jun 1995 1.72181715 177.9441542

#> Jul 1995 -0.90327287 38.6630924

#> Aug 1995 19.24343341 -91.8695239

#> Sep 1995 12.98392759 -158.4336488

#> Oct 1995 7.48791268 -8.4058892

#> Nov 1995 5.56224329 -208.5070889

#> Dec 1995 -5.48257264 0.3567992

#> Jan 1996 11.10534893 -35.5770822

#> Feb 1996 -26.12334333 114.6359751

#> Mar 1996 -1.55693776 -22.1188446

#> Apr 1996 4.33889790 101.8179021

#> May 1996 -3.81951112 -26.3719295

#> Jun 1996 4.24187575 165.8542305

#> Jul 1996 10.63101996 -77.4086771

#> Aug 1996 10.48712620 -92.3937880

#> Sep 1996 -0.38102895 -27.5533378

#> Oct 1996 4.86148920 -59.3399688

#> Nov 1996 16.72882611 -12.2285891

#> Dec 1996 -3.54361164 117.9784246

#> Jan 1997 9.46347886 64.1037374

#> Feb 1997 13.16826356 -62.9588508

#> Mar 1997 -2.96640025 -80.7734971

#> Apr 1997 -3.87213575 -86.0489929

#> May 1997 -7.85432656 -216.9238693

#> Jun 1997 -10.56736867 -137.5836518

#> Jul 1997 -7.95541430 -49.3132472

#> Aug 1997 -17.56275428 -58.1652027

#> Sep 1997 -6.90537897 -16.7229304

#> Oct 1997 -5.58541994 48.5993129

#> Nov 1997 -5.36663326 -133.3395796

#> Dec 1997 2.27127133 -26.1965625

#> Jan 1998 9.78454920 65.2386303

#> Feb 1998 -2.08882651 74.8854971

#> Mar 1998 -13.99410460 89.6560285

#> Apr 1998 2.58537288 148.9300424

#> May 1998 -4.41799453 -65.9403481

#> Jun 1998 5.68599861 53.7283179

#> Jul 1998 21.26850459 74.6803067

#> Aug 1998 4.24858441 189.6317084

#> Sep 1998 -16.84281532 -206.0070725

#> Oct 1998 2.49401784 6.4543870

#> Nov 1998 10.72838252 -26.5147403

#> Dec 1998 20.39369263 -44.7344531

#> Jan 1999 4.49453778 -141.0700927

#> Feb 1999 13.91814046 -50.6418882

#> Mar 1999 4.26566547 -26.9761838

#> Apr 1999 1.07583992 -108.5154918

#> May 1999 0.22294733 36.2159127

#> Jun 1999 6.03611011 -33.5672143

#> Jul 1999 -2.62650573 136.3804498

#> Aug 1999 -5.28264082 -71.1524136

#> Sep 1999 1.92149422 66.2178797

#> Oct 1999 -11.46199669 29.1130223

#> Nov 1999 8.46184665 19.7958000

#> Dec 1999 0.81719629 -120.3566106

#> Jan 2000 -13.05117010 -3.9817044

#> Feb 2000 -9.44912060 68.6982465

#> Mar 2000 4.54341594 70.5267007

#> Apr 2000 -8.55202501 99.1441680

#> May 2000 -2.86895219 114.4248971

#> Jun 2000 8.94961626 -123.8910243

#> Jul 2000 0.67304440 265.4898333

#> Aug 2000 -1.62676337 -15.6917189

#> Sep 2000 -8.27310169 -42.3490117

#> Oct 2000 18.76505621 -19.8387058

#> Nov 2000 7.66440199 -89.4802407

#> Dec 2000 9.79956696 90.4269119

#> Jan 2001 13.21780992 7.9649210

#> Feb 2001 -11.19710829 -125.8827223

#> Mar 2001 5.14599819 102.5685106

#> Apr 2001 -15.09099836 -73.0778603

#> May 2001 15.32741480 -19.0145507

#> Jun 2001 4.29147371 52.8864693

#> Jul 2001 1.22103414 55.0210535

#> Aug 2001 -11.38012401 54.9684337

#> Sep 2001 -5.58015129 -65.9542372

#> Oct 2001 10.52538537 5.7421706

#> Nov 2001 6.77683644 -280.8010508

#> Dec 2001 0.38499547 -91.2259753

#> Jan 2002 -3.56381187 -78.2379163

#> Feb 2002 7.82844102 -66.4104924

#> Mar 2002 8.04411616 62.6309770

#> Apr 2002 -19.00060823 -50.7248206

#> May 2002 9.35784286 27.0361335

#> Jun 2002 -3.09051503 46.7476865

#> Jul 2002 2.63066677 72.3994958

#> Aug 2002 -17.90591856 61.3836939

#> Sep 2002 -7.88258845 -61.7869202

#> Oct 2002 -11.33021669 22.0724902

#> Nov 2002 3.63652568 112.7926598

#> Dec 2002 -2.85887914 181.3454336

#> Jan 2003 5.17669134 -8.3825685

#> Feb 2003 -1.02908670 136.7706666

#> Mar 2003 -9.74069593 -62.7434620

#> Apr 2003 12.70672301 -21.6629150

#> May 2003 9.60864787 -68.3713824

#> Jun 2003 7.68721370 -44.4702734

#> Jul 2003 10.35930771 60.6489806

#> Aug 2003 -4.73887074 62.4183075

#> Sep 2003 -12.75334875 -69.5431074

#> Oct 2003 -3.05620674 -78.3639078

#> Nov 2003 22.11769487 -95.3123859

#> Dec 2003 -10.41668381 179.2756071

#> Jan 2004 -11.46523850 34.8976696

#> Feb 2004 -16.75327303 25.9103768

#> Mar 2004 15.25938655 -80.5951897

#> Apr 2004 5.54185515 10.5664701

#> May 2004 19.93110265 -33.3599682

#> Jun 2004 -1.54120740 164.1847970

#> Jul 2004 25.64408338 -64.3905859

#> Aug 2004 10.61999145 58.7020562

#> Sep 2004 11.42694878 -15.0403088

#> Oct 2004 11.23838843 -171.0821848

#> Nov 2004 -3.97001493 143.1032558

#> Dec 2004 -8.23261151 -264.5212268

#> Jan 2005 -5.78884625 -103.2457405

#> Feb 2005 17.63789378 -70.7466431

#> Mar 2005 1.32992146 -70.0560014

#> Apr 2005 3.76499328 53.7885439

#> May 2005 11.38707653 -31.6332175

#> Jun 2005 12.41263075 -83.9622754

#> Jul 2005 6.12090945 -135.4928062

#> Aug 2005 -4.29380087 -81.7568272

#> Sep 2005 13.60461327 -63.4400003

#> Oct 2005 -0.70857431 81.5949433

#> Nov 2005 -2.72153684 30.2795706

#> Dec 2005 -24.46680029 180.7086625

#> Jan 2006 0.65486641 -89.4026756

#> Feb 2006 -10.98508902 -4.6428211

#> Mar 2006 -6.33178176 -47.1179138

#> Apr 2006 -20.63654451 -52.6692630

#> May 2006 26.48932029 -9.5134908

#> Jun 2006 -11.53398386 -249.5364809

#> Jul 2006 -3.40637876 16.6889217

#> Aug 2006 7.86362576 35.0492384

#> Sep 2006 -12.70513110 143.3701009

#> Oct 2006 5.42141549 76.5906803

#> Nov 2006 0.75105900 116.7520670

#> Dec 2006 5.58514422 -13.6943429

#> Jan 2007 4.15406399 -51.4902044

#> Feb 2007 -14.52299769 151.9744468

#> Mar 2007 9.41206122 -32.8491678

#> Apr 2007 -3.38935872 -5.3671506

#> May 2007 -0.75574247 -56.3524635

#> Jun 2007 0.40204392 -74.3908963

#> Jul 2007 1.24301066 -10.9041651

#> Aug 2007 -9.98432551 -56.0829227

#> Sep 2007 12.33390065 18.8001549

#> Oct 2007 3.40424488 74.8850942

#> Nov 2007 -4.72702482 -191.6538316

#> Dec 2007 7.08753061 23.6095847

#> Jan 2008 -15.28958715 62.8953415

#> Feb 2008 2.37425345 41.7925676

#> Mar 2008 -13.12814246 197.6758477

#> Apr 2008 7.47028587 -50.6286298

#> May 2008 -15.62518435 -110.9968853

#> Jun 2008 0.71053360 -94.8705723

#> Jul 2008 -6.39534770 47.6843757

#> Aug 2008 -8.45195739 -79.5201560

#> Sep 2008 6.75244698 23.4326923

#> Oct 2008 11.53375794 -122.2451097

#> Nov 2008 -16.86504742 -245.3647354

#> Dec 2008 -9.02814949 -148.9260814

#> Jan 2009 13.17633698 -43.2147734

#> Feb 2009 11.00189745 -94.2554006

#> Mar 2009 12.03767839 -12.1450799

#> Apr 2009 -14.31270777 133.6446798

#> May 2009 13.82910861 -86.0356182

#> Jun 2009 0.03125940 66.6537820

#> Jul 2009 -0.77886824 -142.1534746

#> Aug 2009 4.41428226 117.0056168

#> Sep 2009 1.28922896 -140.4714543

#> Oct 2009 -8.30214260 110.1708096

#> Nov 2009 -5.03592910 69.7986263

#> Dec 2009 -11.93641182 -86.4349803

#> Jan 2010 -7.51723323 -109.1470351

#> Feb 2010 14.55841403 -3.7051465

#> Mar 2010 -8.28603533 81.0053792

#> Apr 2010 2.89774460 -49.9355412

#> May 2010 -4.80053484 94.8031588

#> Jun 2010 -6.04829354 -17.4245957

#> Jul 2010 14.60110180 -110.6235952

#> Aug 2010 1.49679354 -94.5985005

#> Sep 2010 -14.33321100 28.9089591

#> Oct 2010 -0.10303319 87.6913145

#> Nov 2010 -2.12236035 -114.8903940

#> Dec 2010 -9.06340179 -113.7612756

#> Jan 2011 -21.02152479 -143.7246735

#> Feb 2011 18.93360464 -49.4143476

#> Mar 2011 -9.68125837 84.0801808

#> Apr 2011 -1.02603036 79.1534124

#> May 2011 2.39959572 -16.8848948

#> Jun 2011 0.60898893 61.2722104

#> Jul 2011 -21.77576028 -77.1158924

#> Aug 2011 -1.17860143 88.8628993

#> Sep 2011 1.12294787 1.3214477

#> Oct 2011 0.07886198 22.5339515

#> Nov 2011 18.77743872 -72.9915210

#> Dec 2011 21.58756554 -122.2487070

#> Jan 2012 7.09714522 40.6805171

#> Feb 2012 7.66983379 -75.1012223

#> Mar 2012 -3.08211421 -16.2116540

#> Apr 2012 10.12001849 35.2010126

#> May 2012 -9.19051597 -28.9058300

#> Jun 2012 5.63380077 10.4662227

#> Jul 2012 3.22482749 72.0186531

#> Aug 2012 3.66674363 -61.1046082

#> Sep 2012 11.29835153 -110.6914072

#> Oct 2012 -9.41498076 53.4803326

#> Nov 2012 2.17837643 73.6067968

#> Dec 2012 14.15412293 -122.2501574

#> Jan 2013 -3.83733048 102.1415310

#> Feb 2013 -1.74086374 46.5165158

#> Mar 2013 -2.21744517 79.0472705

#> Apr 2013 -10.09528722 -13.0264801

#> May 2013 4.80725266 -93.0285334

#> Jun 2013 16.04407328 -36.4851004

#> Jul 2013 -15.15024529 15.3872493

#> Aug 2013 -14.16023914 41.3154818

#> Sep 2013 8.76777327 248.0823360

#> Oct 2013 6.24132413 -217.9956742

#> Nov 2013 21.12277288 42.0874578

#> Dec 2013 -3.56124416 -35.7528325

#> Jan 2014 -10.64464209 -64.6861514

#> Feb 2014 10.77116538 -5.0141801

#> Mar 2014 11.81575567 41.6942847

#> Apr 2014 1.98392095 -63.2587542

#> May 2014 -4.00405249 115.0146673

#> Jun 2014 6.16154281 -23.5475907

#> Jul 2014 19.74156748 -164.3107386

#> Aug 2014 18.84662324 -150.3382146

#> Sep 2014 -15.88620547 -205.0584847

#> Oct 2014 -5.39923164 -75.3198229

#> Nov 2014 -11.69461464 -13.4141958

#> Dec 2014 5.59105989 100.5782847

#> Jan 2015 -18.19347247 216.7186798

#> Feb 2015 3.93343972 232.2556540

#> Mar 2015 0.42134106 -102.0423391

#> Apr 2015 11.79664177 4.8814436

#> May 2015 -2.56921176 -77.1888628

#> Jun 2015 -10.56336098 -78.5235068

#> Jul 2015 1.98777205 -72.6603031

#> Aug 2015 6.50533552 68.1878032

#> Sep 2015 3.43913337 -22.9843287

#> Oct 2015 14.77532312 -151.0601724

#> Nov 2015 0.72025698 -58.3727687

#> Dec 2015 21.26444534 -202.2918454

#> Jan 2016 -14.76196906 40.3504676

#> Feb 2016 4.07888500 55.0015549

#> Mar 2016 13.93977798 2.8357122

#> Apr 2016 3.60278296 89.3165020

#> May 2016 6.54550251 -37.6555496

#> Jun 2016 10.52155422 60.5884808

#> Jul 2016 -19.79555125 -0.4874726

#> Aug 2016 12.08385605 -52.0796373

#> Sep 2016 -1.69280084 -63.9018598

#> Oct 2016 2.95029753 -63.5894137

#> Nov 2016 12.66340587 10.6586975

#> Dec 2016 -11.35343257 117.6914248

#> Jan 2017 -11.31053798 44.7391153

#> Feb 2017 1.09993384 227.2954766

#> Mar 2017 8.52905410 13.6058206

#> Apr 2017 -2.34337862 -199.9039133

#> May 2017 20.86688567 -42.0500870

#> Jun 2017 -1.10919371 -37.8407395

#> Jul 2017 -13.92847056 122.0774789

#> Aug 2017 -11.42290768 -154.1030292

#> Sep 2017 17.04608737 -31.0310122

#> Oct 2017 -0.80073634 -2.0108184

#> Nov 2017 -4.37281240 -239.0200336

#> Dec 2017 -1.19215094 88.9865359

#> Jan 2018 7.86462865 -148.2813325

#> Feb 2018 -5.78945246 44.5750348

#> Mar 2018 -1.45426885 136.9775856

#> Apr 2018 5.26457991 -2.0110027

#> May 2018 17.33578110 -10.9217587

#> Jun 2018 14.48657220 26.4661745

#> Jul 2018 15.18193149 30.3848264

#> Aug 2018 -3.84007254 -18.3388483

#> Sep 2018 18.27125177 55.9649672

#> Oct 2018 -5.51491750 -18.6553842

#> Nov 2018 -8.65753541 -81.2275372

#> Dec 2018 -3.43831481 -164.0581672

#> Jan 2019 10.62876458 50.7922478

#> Feb 2019 8.13058204 175.4336961

#> Mar 2019 18.03483361 59.2400202

#> Apr 2019 -1.05068694 101.6713288

#> May 2019 9.82453362 12.1620586

#> Jun 2019 -17.13302622 -107.8067265

#> Jul 2019 -8.32019527 -114.3565720

#> Aug 2019 11.00491882 -52.9643677

#> Sep 2019 -1.73820106 -68.1273156

#> Oct 2019 1.78812018 -20.2447559

#> Nov 2019 -6.98429449 168.4495721

#> Dec 2019 -9.60449159 -103.3773237

#> Jan 2020 -9.75423042 -15.5976673

#> Feb 2020 -3.38576503 -4.6400637

#> Mar 2020 11.52347074 -95.3628727

#> Apr 2020 4.05101183 41.6260798

#> May 2020 -4.70922497 11.4029609

#> Jun 2020 -1.33251019 6.3918753

#> Jul 2020 12.26682356 -91.9332238

#> Aug 2020 3.32943995 90.1335290

#> Sep 2020 -3.47088466 -79.7728297

#> Oct 2020 -0.98550690 66.8221204

#> Nov 2020 0.34766060 15.5214296

#> Dec 2020 3.86127022 12.8688092

#>

#> $description

#> type coeff

#> var1 Undefined NA

#> var2 Undefined NA

#>

myreg3 <- regarima(myseries, myspec3)

myreg3

#> y = regression model + arima (2, 1, 0, 1, 1, 1)

#> Log-transformation: no

#> Coefficients:

#> Estimate Std. Error

#> Phi(1) 0.4744 0.051

#> Phi(2) 0.3312 0.051

#> BPhi(1) -0.2569 0.072

#> BTheta(1) -0.8066 0.043

#>

#> Estimate Std. Error

#> r.var1 0.016274 0.009

#> r.var2 0.001222 0.001

#> Week days 0.689237 0.036

#> Leap year 2.054858 0.662

#> Easter [6] -2.509781 0.411

#> TC (4-2020) -22.552758 2.120

#> TC (3-2020) -21.119937 2.128

#> AO (5-2011) 12.809939 1.739

#> LS (1-2009) -9.611835 1.796

#>

#>

#> Residual standard error: 2.244 on 345 degrees of freedom

#> Log likelihood = -803.6, aic = 1635 aicc = 1636, bic(corrected for length) = 1.829

#>

# }