Defining a Basic Structural Model with rjd3sts

The package allows several equivalent definitions of a basic structural model. We present below some of them.

To compare the results (more precisely the likelihood) of the different approaches, it is important to compute the marginal likelihood.

s<-log(Retail$BookStores)Standard definition, noise in the state

# create the model

bsm<-model()

# create the components and add them to the model

add(bsm, locallineartrend("ll"))

add(bsm, seasonal("s", 12, type="HarrisonStevens"))

add(bsm, noise("n"))

rslt<-estimate(bsm, s, marginal=TRUE)- Likelihood = 349.1426991

- Parameters = 0.168604, 0.000382, 0.271294, 1.000000

Standard definition, noise in the measurement

# create the model

bsm<-model()

# create the components and add them to the model

add(bsm, locallineartrend("ll"))

add(bsm, seasonal("s", 12, type="HarrisonStevens"))

# create the equation (fix the variance to 1)

eq<-equation("eq", 1,TRUE)

add_equation(eq, "ll")

add_equation(eq, "s")

add(bsm, eq)

rslt<-estimate(bsm, s, marginal=TRUE)- Likelihood = 349.1426991

- Parameters = 0.168604, 0.000382, 0.271294, 1.000000

components with fixed variances, aggregated with diffuse weights (noise in the state)

# create the model

bsm<-model()

# create the components, with fixed variances, and add them to the model

add(bsm, locallineartrend("ll",

levelVariance = 1, fixedLevelVariance = TRUE))

add(bsm, seasonal("s", 12, type="HarrisonStevens",

variance = 1, fixed = TRUE))

add(bsm, noise("n", 1, fixed=TRUE))

# create the equation (fix the variance to 1)

eq<-equation("eq", 0, TRUE)

add_equation(eq, "ll", .01, FALSE)

add_equation(eq, "s", .01, FALSE)

add_equation(eq, "n")

add(bsm, eq)

rslt<-estimate(bsm, s, marginal=TRUE)

p<-result(rslt, "parameters")- Likelihood = 349.1426991

- Parameters = 1.0000, 0.0023, 1.0000, 1.0000, 0.4106, 0.5209

To be noted:

- Level variance = = 0.168622

- Slope variance = = 0.000382

- Seas variance = = 0.271323

bsm with long term trend and cycle

# create the model

bsm<-model()

# create the components and add them to the model

add(bsm, locallevel("l", initial = 0))

add(bsm, locallineartrend("lt", levelVariance = 0,

fixedLevelVariance = TRUE))

add(bsm, seasonal("s", 12, type="HarrisonStevens"))

add(bsm, noise("n", 1, fixed=TRUE))

# create the equation (fix the variance to 1)

rslt<-estimate(bsm, s, marginal=TRUE)- Likelihood = 349.1426991

- Parameters = 0.168604, 0.000000, 0.000382, 0.271294, 1.000000

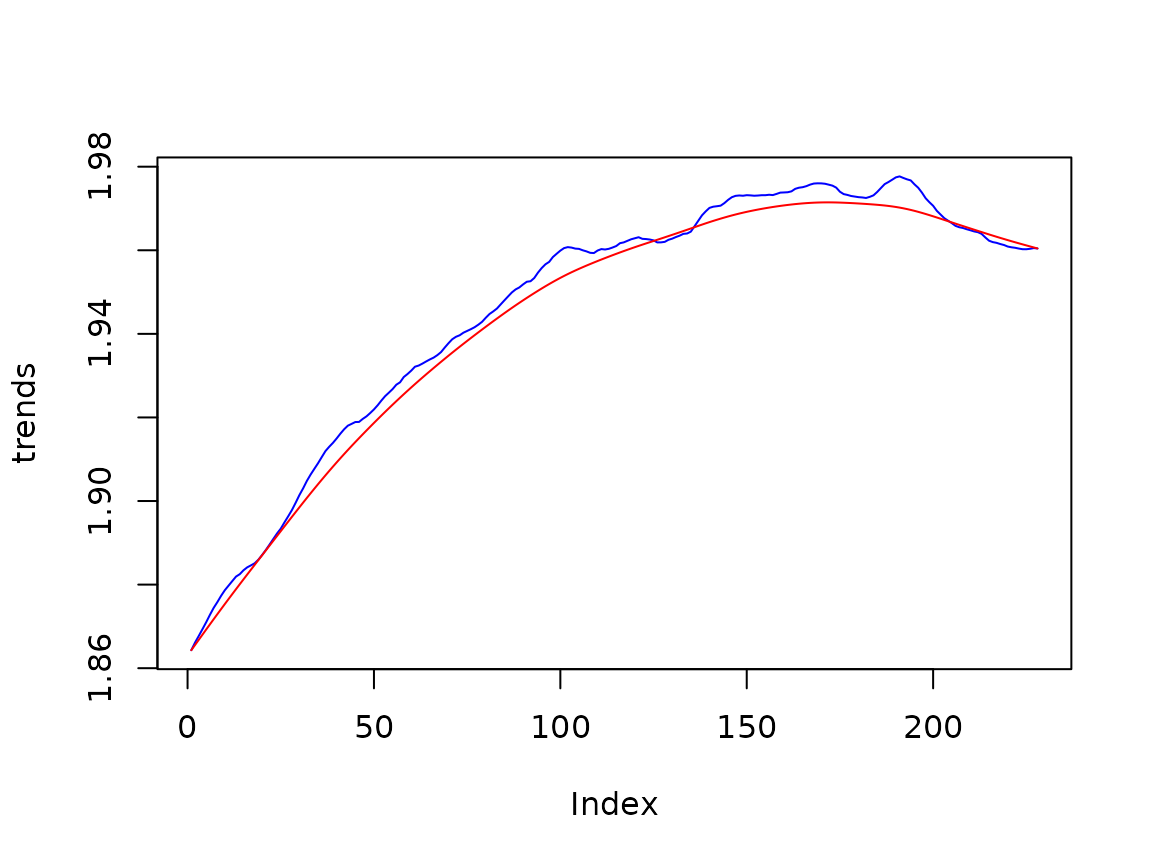

ss<-smoothed_states(rslt)

plot(ss[,1]+ss[,2], type='l', col='blue', ylab='trends')

lines(ss[, 2], col='red')