Introduction

This document presents some results on time-dependent arima models developed by G. Melard et al., as they are implemented in JDemetra+ The current implementation focuses on airline models.

Estimation of time-dependent airline models

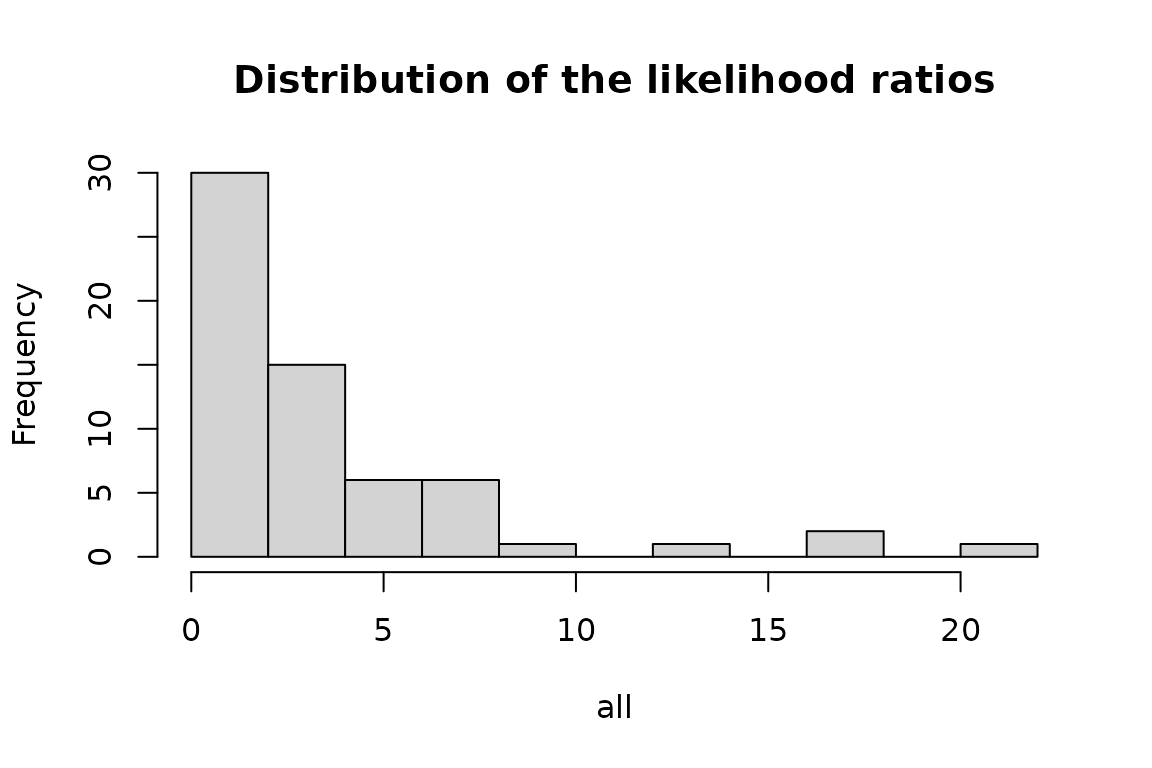

The likelihood ratios between time-dependent and normal airline models computed on 62 series of the US-retail trade statistics are presented below. Likelihood ratios above 4 indicate a significant preference for the time-dependent models.

test<-function(z){

q<-rjd3sts::tdairline_estimation(z)

return (q$ltd_sarima$likelihood- q$sarima$likelihood)

}

all<-sapply(rjd3toolkit::Retail, function(z) test(z))

hist(all, breaks=10, main="Distribution of the likelihood ratios")

print(all)

#> AllOtherGenMerchandiseStores AllOtherHomeFurnishingsStores

#> 0.2599687 1.8073763

#> AppltvAndOtherElectStores AutomobileDealers

#> 2.6904441 7.5012325

#> BeerWineAndLiquorStores BookStores

#> 1.4763512 2.4879537

#> BuildingMatAndGardenEquipAndSupp BuildingMatAndSuppliesDealers

#> 1.8481865 0.9798839

#> ClothingAndClothingAccessStores ClothingStores

#> 3.0727796 1.9433920

#> ComputerAndSoftwareStores DepartmentStoresExclDiscountDepa

#> 0.3787791 7.2711916

#> DepartmentStoresExclLD DepartmentStoresInclLD

#> 0.8590355 0.7634333

#> DiscountDeptStoresInclLD DiscountDeptStores

#> 4.8956456 5.5606961

#> DrinkingPlaces ElectronicsAndApplianceStores

#> 0.6082423 1.7897230

#> FamilyClothingStores FloorCoveringStores

#> 5.3726852 1.5696636

#> FoodAndBeverageStores FoodServicesAndDrinkingPlaces

#> 5.9461737 0.5840378

#> FuelDealers FullServiceRestaurants

#> 0.8083703 0.2150196

#> FurnitureAndHomeFurnishingsStore FurnitureHomeFurnElectronicsAndA

#> 2.3809754 2.0432794

#> FurnitureStores Gafo

#> 1.9144394 3.8209734

#> GasolineStations GeneralMerchandiseStores

#> 13.9093037 5.9325953

#> GiftNoveltyAndSouvenirStores GroceryStores

#> 1.4066652 5.1526660

#> HardwareStores HealthAndPersonalCareStores

#> 0.9931652 7.3192726

#> HobbyToyAndGameStores HomeFurnishingsStores

#> 2.8548124 3.0032888

#> HouseholdApplianceStores JewelryStores

#> 0.6237299 1.4549538

#> LimitedServiceEatingPlaces MensClothingStores

#> 0.8227719 0.7571241

#> MiscellaneousStoreRetailers MotorVehicleAndPartsDealers

#> 0.7306779 8.6937372

#> NewCarDealers NonstoreRetailers

#> 6.6432701 0.7205383

#> OfficeSuppliesAndStationeryStore OfficeSuppliesStationeryAndGiftS

#> 2.3736957 0.2937239

#> OtherClothingStores OtherGeneralMerchandiseStores

#> 1.0651051 3.4746228

#> PaintAndWallpaperStores PharmaciesAndDrugStores

#> 0.4836048 6.8507426

#> RadioTVAndOtherElectStores RetailAndFoodServicesSalesTotal

#> 3.4329575 17.3490489

#> RetailSalesTotalExclMotorVehicle RetailSalesTotal

#> 21.4911139 17.7320144

#> ShoeStores SportingGoodsHobbyBookAndMusicSt

#> 6.3539561 2.9775295

#> SportingGoodsStores SupermarketsAndOtherGroceryExcep

#> 0.2488864 0.1707006

#> UsedCarDealers UsedMerchandiseStores

#> 3.1951571 3.1441175

#> WarehouseClubsAndSuperstores WomensClothingStores

#> 3.0298947 1.1010737Canonical decomposition and estimation of the components by means of the Kalman smoother

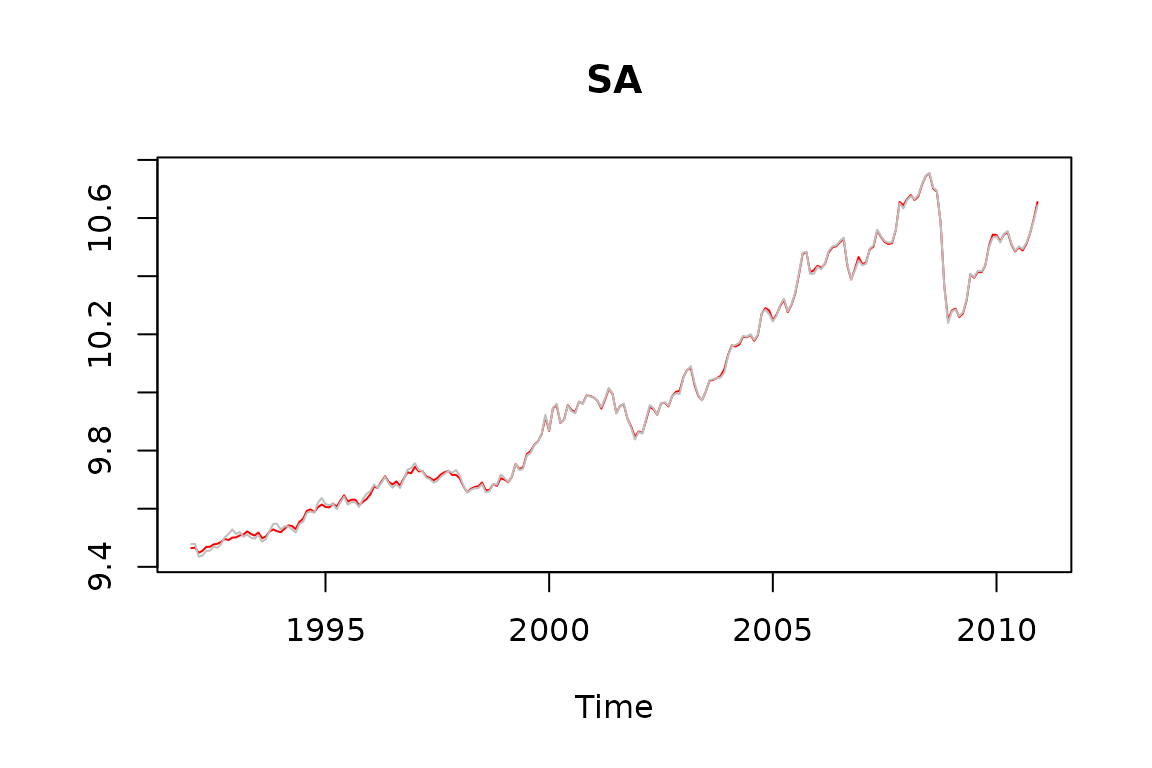

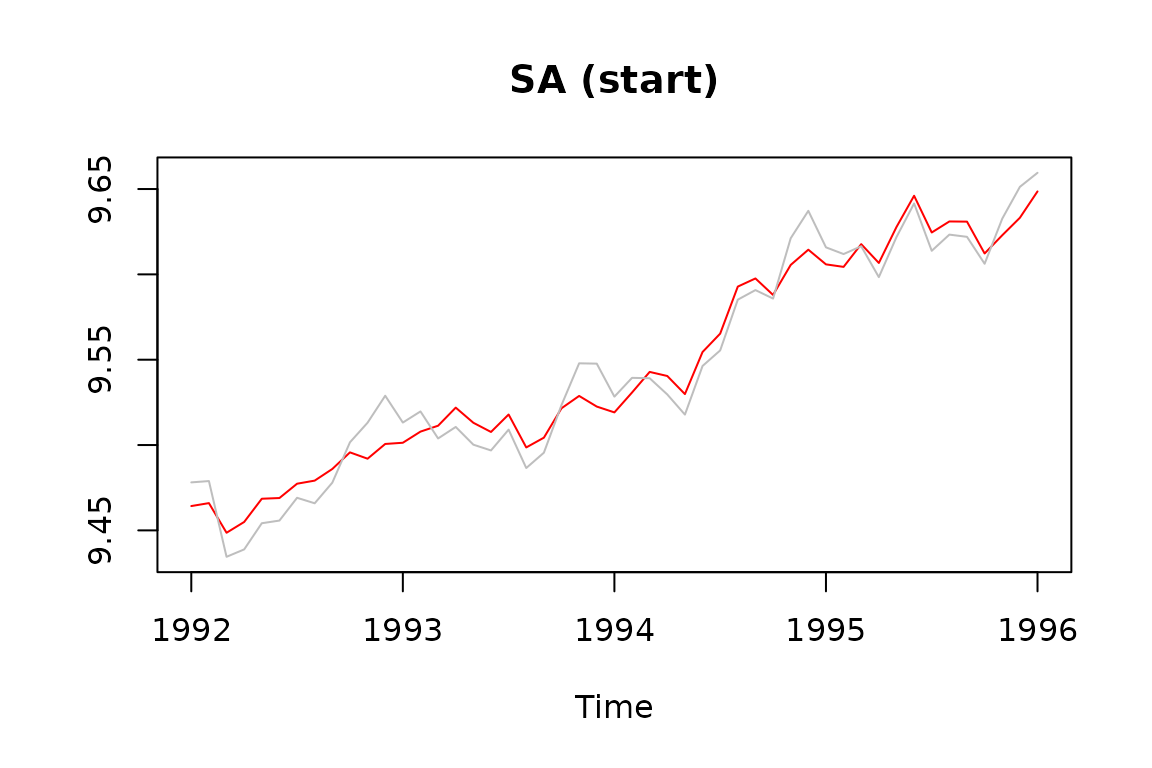

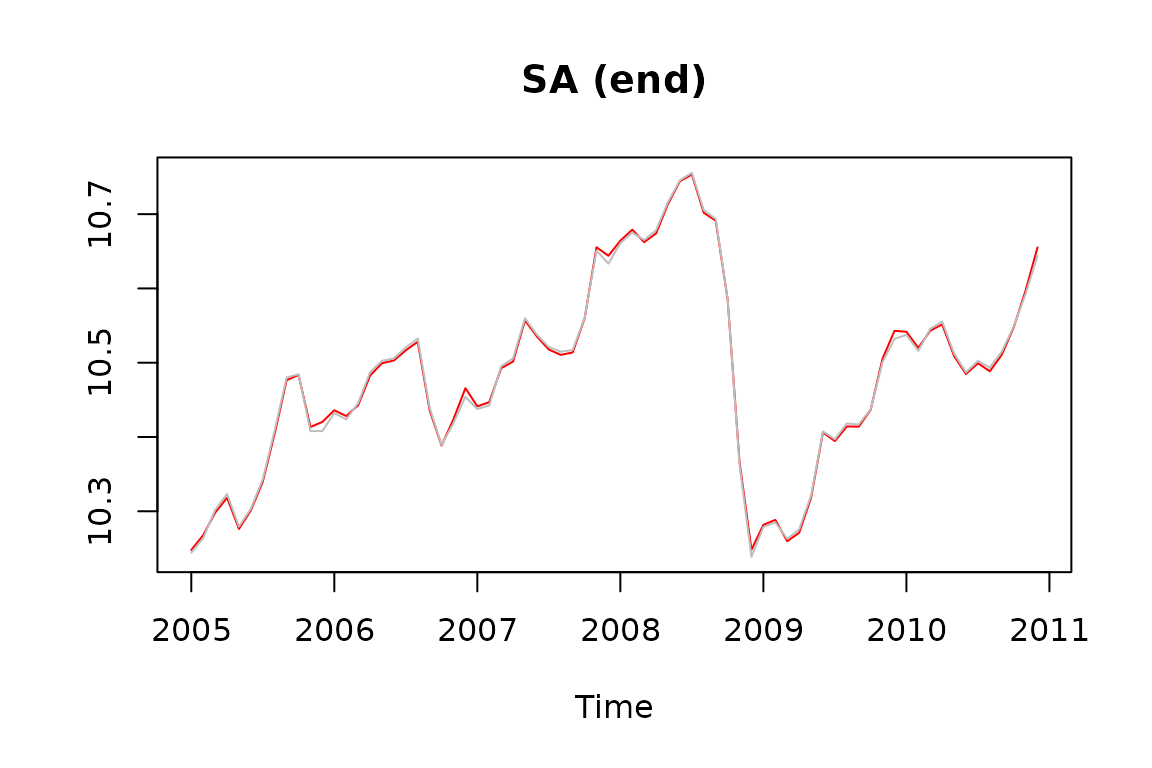

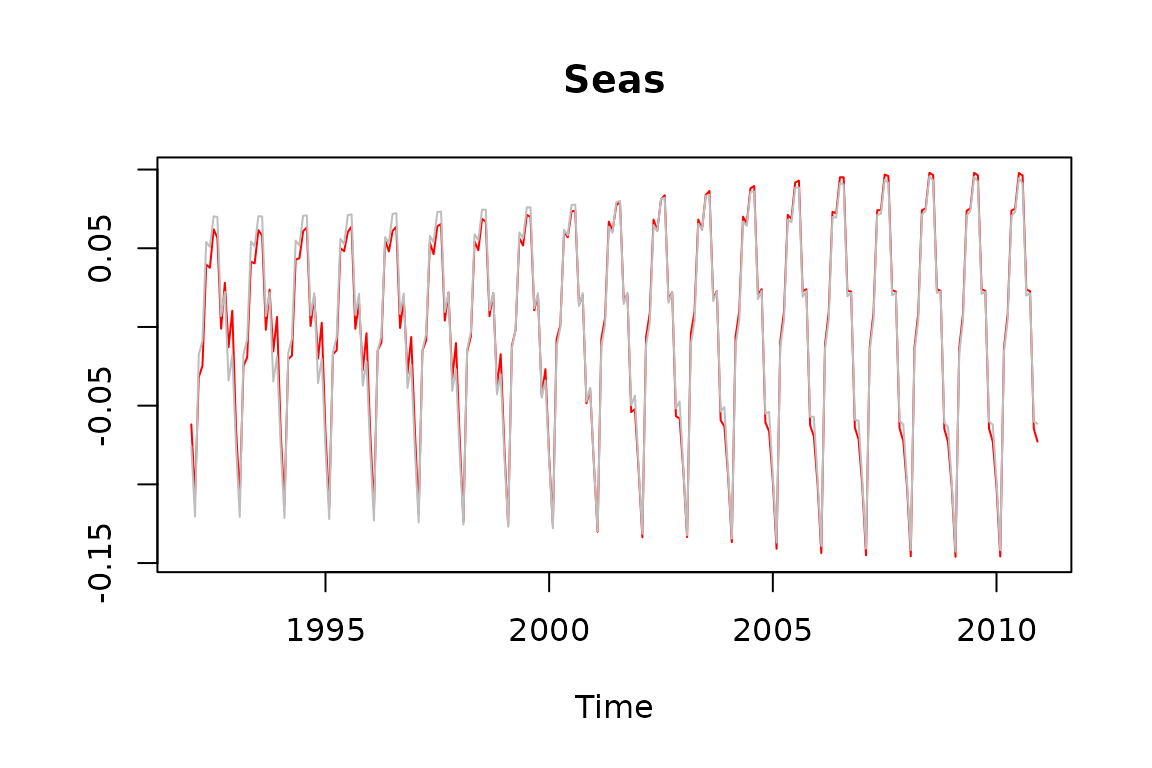

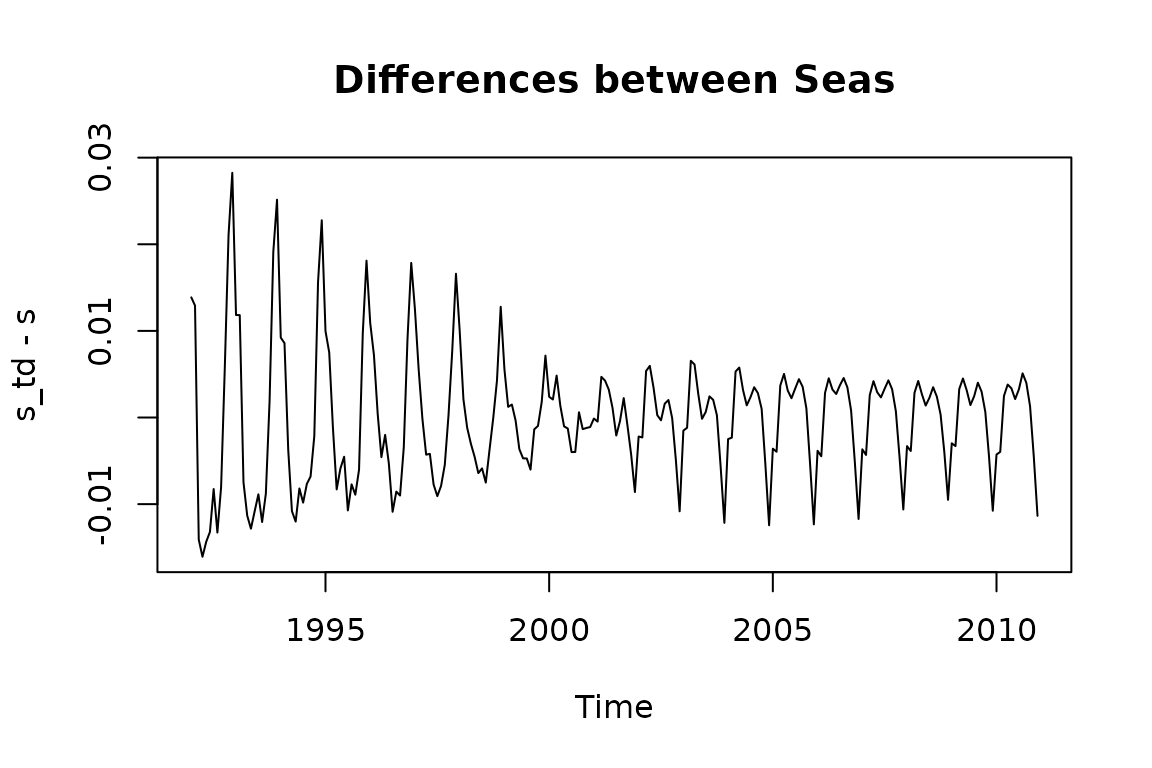

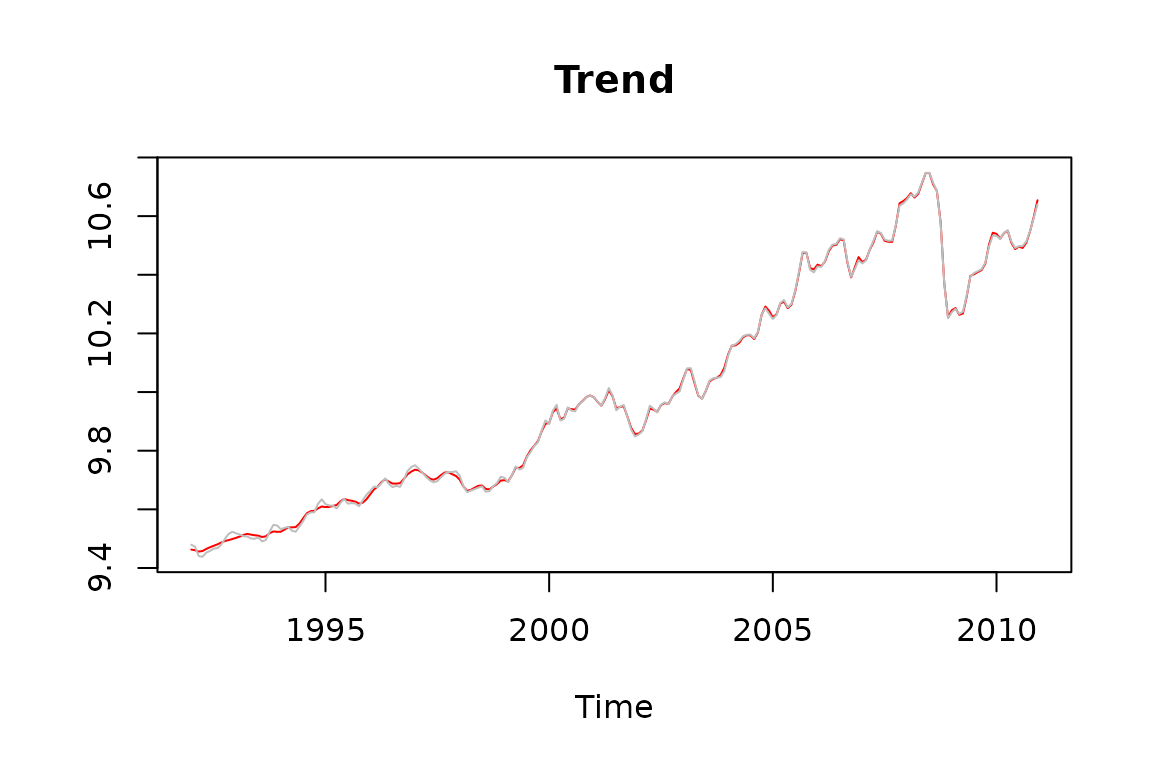

We present below the seasonal adjustment of a series (retail trade of gasoline stations) and the differences between the series based on the airline model and the time-dependent airline model, using the Kalman smoother (time-dependent series in red)

s<-log(rjd3toolkit::Retail$GasolineStations)

q<-rjd3sts::tdairline_estimation(s)

tdss<-rjd3sts::tdairline_decomposition(s, q$ltd_sarima$parameters)

Main results

Airline:

log-likelihood = 400.3207451

0.3963676

-0.8673957

Time-dependent airline

log-likelihood = 413.0957868

0.2413694 [ -0.1347973, 0.6175361]

-0.7274294 [ -0.4548589, -1]

Canonical decomposition

airline_decomposition<-function(period, th, bth){

sarima<-rjd3toolkit::sarima_model("m", period, NULL, 1, th, NULL, 1, bth)

return (rjd3tramoseats::seats_decompose(sarima))

}

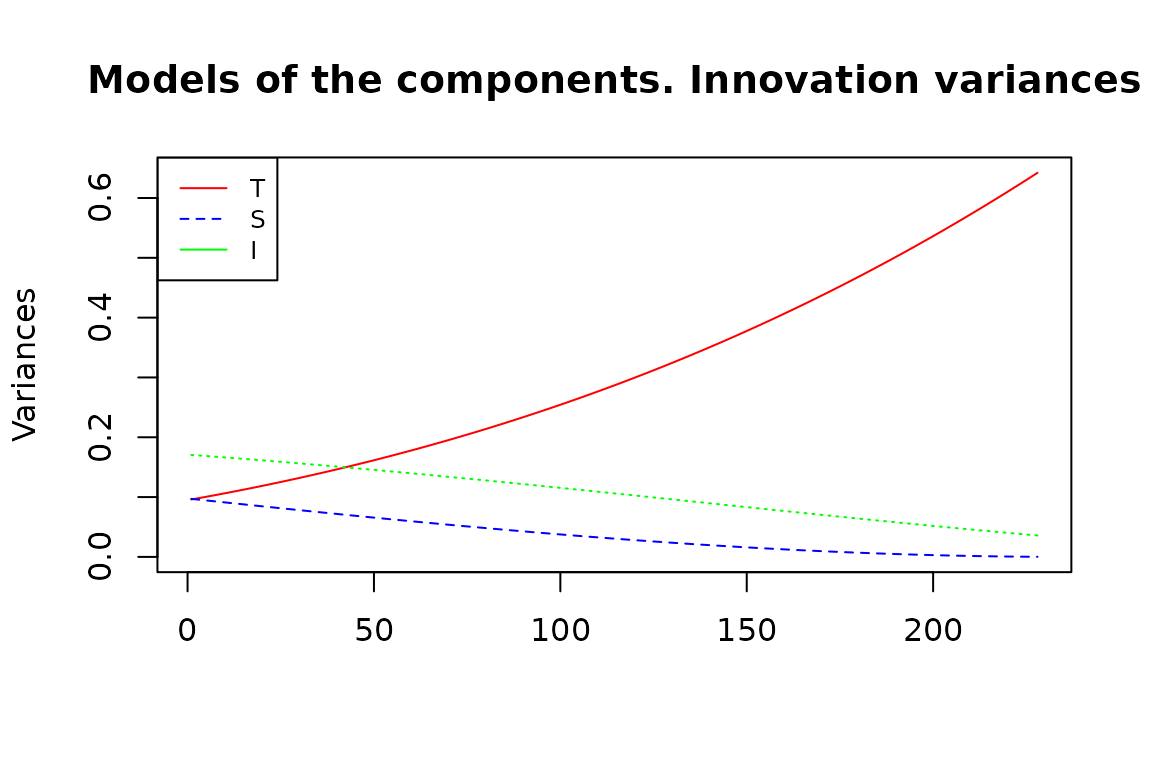

airline_variances<-function(period, th, bth){

ucm<-airline_decomposition(period, th, bth)

if (is.null(ucm)) return (c(NA, NA, NA)) else return (c(ucm$components[[1]]$var,

ucm$components[[2]]$var,

ucm$components[[3]]$var))

}

# Gets the variances of the canonical decomposition for airline models with different parameters

th<-q$ltd_sarima$th

bth<-q$ltd_sarima$bth

vars<-sapply(seq(1, length(th)), function(z){return (airline_variances(12,th[z], bth[z]))})

vars<-t(vars)

matplot(vars, main="Models of the components. Innovation variances", type = 'l', ylab="Variances",col=c("red", "blue", "green"))

legend("topleft", legend=c("T", "S", "I"),

col=c("red", "blue", "green"), lty=1:2, cex=0.8)